Chatswood serves the life and health insurance sector in New Zealand with market intelligence, data, and bespoke consulting services. Some of these are provided in conjunction with Quality Product Research Limited - a subsidiary that brings you Quotemonster.

We believe that good decisions are more likely to occur when we have good information about the market environment in which we operate. Intuitive leaps and creative decisions are always required, of course, but the more they are based on a firm foundation of observation, the better they tend to be.

Quality Product Research: Major Review of Trauma Incidence

According to the FSC, in 2020, a total of $113,700,000 trauma claims were paid out in New Zealand, accounting for 20% of risk claims paid out at the time. Quality Product Research (QPR) uses reinsurer claims information to weight our scoring according to the most important items. For example, 80-90% of our trauma weighting is given to high claiming conditions and the remaining is evenly distributed between minor conditions.

Our incidence factor aims to reflect how likely a benefit will be claimed and is vital within trauma, currently females have an incidence of 69.17% for cancer, while this number is 43.46% in males. Failing to consider this factor would affect the value of certain benefits - we aim to have the incidence rate in our model closely track actual claims to provide a real value-based approach to rating.

Our four-factor research considers four features in our overall score:

Definition x Incidence x Amount x Frequency = Insurance Quality Score

For more information on our methodology please click here.

Based on the most recent claims data from Gen Re, we have reviewed our Trauma Incidence Scores and openly welcome your feedback on these. Please find attached:

A comparison of current and proposed trauma incidence – click here to view (excel file).

A trauma incidence infographic – click here to view (pdf).

Your feedback

We value getting your feedback on how these wordings are being applied to claims you may be aware of. Please email us with details of any recent claims to assist with our ratings.

Doreen Dutt, Quality Product Research Limited, researcher@qpresearch.co.nz

Legal and regulatory update for the life and health insurance sector

9 Jun 2023 - ASIC has granted relief to life and general insurers to provide modifications and exemptions from the confirmation of transaction requirements contained in section 1017F of the Corporations Act in prescribed circumstances. The relief will expire on 1 July 2028.

Confirming transactions – deceased life insurance policyholder

This relief seeks to address situations where it may not be appropriate and/or necessary to confirm transactions with the holder of a life insurance policy where the life insurance policyholder is deceased and there is no alternative holder of the product.

Confirming transactions – recurring insurance benefit payments

For certain recurring benefit claims, this relief seeks to facilitate life and general insurers providing confirmation in the form of a statement given before, rather than after, the transactions are made. This includes benefit payments where the holder of the product is unable to work because of illness, injury or unemployment.

13 Jun 2023 - ASIC invites Australian entities to take part in the ASIC cyber pulse survey to measure cyber resilience https://asic.gov.au/about-asic/news-centre/find-a-media-release/2023-releases/23-160mr-asic-invites-australian-entities-to-assess-their-cyber-resilience/

13 Jun 2023 - NZ Police Financial Intelligence Unit released “The Suspicious Activity Report” for April 2023 https://www.police.govt.nz/sites/default/files/publications/fiu-monthly-report-apr2023.pdf

13 Jun 2023 - The Reserve Bank of New Zealand has released its finalised risk weighting decisions and response to the points raised in submissions. They have also published an Exposure Draft of the associated Banking Prudential Requirements (BPR) document that covers the technical changes needed to implement the decisions. https://www.rbnz.govt.nz/hub/news/2023/06/further-decisions-on-bank-risk-weights-released

14 Jun 2023 - Minister of Finance, Hon Grant Robertson, May 2023 diary released with the following potential financial services sector related meeting noted:

• 1 May 2023 – Ministerial meeting with RBNZ officials, Treasury officials

• 12 May 2023 – Speech at BNZ pre-Budget event

• 12 May 2023 – Speech at Centre for Sustainable Finance CEO roundtable

• 19 May 2023 - Speech at ANZ post-Budget event

• 22 May 2023 – Meeting with RBNZ

• 24 May 2023 - Call with RBNZ

https://www.beehive.govt.nz/sites/default/files/2023-06/Ministerial%20Diary%20May%202023.pdf

Quality Product Research: FAQ – can research ratings be altered?

We hope this explanation can provide more clarity on how our research works.

Our objective is to be a tool for advisers to highlight the material differences between products, rather than a view of ranking them from best to worse, therefore, advisers are able to select their product and provider basket to what they are qualified to advise on (i.e., they can remove providers and alter products where required). However, in reality, price is also a significant factor during the advice process and both our pricing comparison and research rating are used by advisers to justify why a selection is being made - along with other information and views you may have, of course.

For example, ideally an adviser will select all agreed value base products under non-taxable (agreed value).

In this set, Partners Life may have a research rating advantage, but pricing disadvantage, assuming current settings.

If an adviser then decides they want to remove Partners, for whatever reason (perhaps they have no accreditation with them), this removes Partners Life from being shown in the premium comparison however, it would be inaccurate to then bump AIA to 100% because in this specific set Partners Life still has the highest score.

When it comes to Options and Extras packages, in an ideal world, an adviser would select the best products in the set to compare and again will have to consider the pricing comparison and research rating as a package.

Fidelity has a pricing advantage (cheapest in this set) and a research advantage in this example below.

However, removing Fidelity will remove the provider from appearing in the premium comparison, but it will not alter the research comparison – they still have the highest rating in the set and the other companies are benchmarked against this.

We believe it would be inaccurate if advisers were allowed to remove a company to then alter research ratings. They can, however, alter products but have to be able to justify it from a pricing and rating perspective.

We hope this provides some insight into how research ratings work and if there is a specific topic you would like us to share on, please send us an email on info@quotemonster.co.nz

Questions answered: does everyone already have a life insurance policy?

Question from a reader:

The FSC have released their quarterly life insurance snapshot FSC SPOTLIGHT Life Insurance MAR 2023.pdf (hubspotusercontent-na1.net). What I found particularly interesting was there are 4.1 million life insurance covers and New Zealand has about 5.18 million residents. Stats NZ has 986600 people under 15 in 2021 national-population-estimates-at-30-june-2021.xlsx (live.com), and I would assume most under 15 year olds wouldn’t have (or need) life insurance. So, are we basically at market saturation now? Or are there a large number of people with multiple life insurance policies?

Answer:

At Chatswood we do not think that everyone has a life policy and you are right to suspect that multiple policies is a likely explanation. For example, at one point I had five policies with Sovereign, that was a consequence of how increases and additions were done. At the same time I had some group life insurance in the staff scheme, so that made it six. I may have had some credit card insurance too. We work on an average of between two and three policies per person, which leaves the uninsured at about 50% of the working age population. The FSC has also recently done a survey of consumers and their answers indicated that the coverage rate is about 38%. However, consumer surveys about low engagement products such as life insurance are particularly susceptible to response biases. I explore some of these issues in my recent article at goodreturns 'why is is so hard to know how many people have life insurance?' If you would like a more detailed approach to this with the associated modelling and sources please contact us for a copy of our special report on market size and flow.

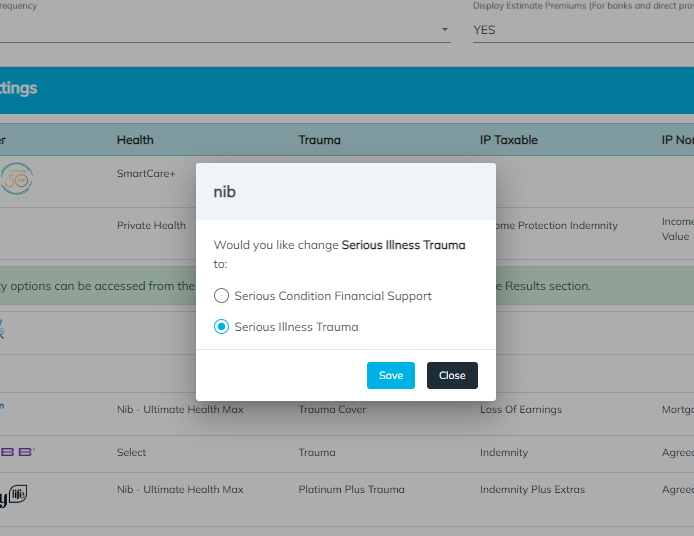

The addition of nib Life & Living to Quotemonster!

We have recently updated Quotemonster to include nibs Life & Living products.

In the Product and Provider Settings, you’ll find the usual options for nib under Health, and now you’ll be able to include Life & Living Life, Trauma and Income Protection in your pricing and research comparisons. This also means that you’ll be able to quote a package for this provider.

Note that we have included both the Serious condition Financial Support option (only available for sum insureds of $20,000 or $50,000) and Serious Illness Cover to select from in Trauma.

Click here to read more on this topic in Insurance Business, which also includes an interview with Chris Carnall, nibs Adviser Distribution Head, and you can click here to register for nibs national roadshow.

If you have any questions or feedback on this topic, please feel free to contact us on info@quotemonster.co.nz

Quality Product Research: Research Ratings Terminology

If you’ve ever seen the terms Total Benefits Score or Total Weighted IQ Rating on Quotemonster and wondered what they meant, you’re not the only one!

Here is some information on numbers and terminology which we hope will provide you with a better understanding of our Research.

For a product (e.g., Life Cover), the Total Benefits Score (Image 1) is the sum total of every benefit being rated. You can view the entire list of benefits by ordering your Research Alphabetically.

Image 1:

The Percentage Rating (Image 1) converts to a Star rating for each insurer’s products and is also provided in this screen.

In the example above (Image 1), the highest total benefits score is 106.44, which belongs to AIA, therefore this company has a Percentage Rating of 100% and is a 5-star product. Next, the other products are benchmarked against this as below:

Chubb Life: 104.76/106.44 = 98.4% rounds to 98%

Fidelity: 104.50/106.44 = 98.2% rounds to 98%

Partners Life: 106.02/106.44 = 99.8%, rounds to 100%

The Percentage Rating is then converted into a Star Rating according to our table below:

When ordering by Importance, we aim to only present the high scoring benefits for the selected product, and all others are combined and displayed in the Secondary Benefits Score (Image 2).

Again, to see every benefit, simply order Alphabetically.

Image 2:

Researchmonster subscribers have the additional Research tab, which defaults to the Package Score and includes the term Total Weighted IQ Rating.

IQ = Insurance Quality and we highly recommend referring to our Why Methodology Matters infographic for detailed information and you can click here to download this.

To get the Total Weighted IQ Rating, the Total Benefits Score for each product is multiplied by the Product Line Weighting Factor*

*In reality, the distribution of claims differs based on age, gender, and other factors. Our Product Line Weighting Factor aims to model the relative weight of a claim and as we know, models aren’t an exact science.

In our example below (Image 3), Chubb Life: 104.76 (Total Benefits Score) x 0.1 (Product Line Weighting Factor) = 10.48 (package score for Life cover).

This is completed for each benefit and totalled to form the Total Weighted IQ Rating (Image 3).

Life 10.48 + Trauma 31.85 + Health 10.42 + Mortgage 14.37 + TPD 14.97 + Income 19.21 = 101.30

Star ratings (aka Percentage Rating) for the package is also provided in this screen.

In this set, the highest score is 102.85, which belongs to Partners Life, therefore this company has a Percentage Rating of 100% and offers a 5-star package suite. Next, the other products are benchmarked against this as below:

AIA: 101.66/102.85 = 99%, Chubb Life: 101.30/102.85 = 98%, Fidelity: 100.01/102.85 = 97%

Image 3:

We hope this provides some insight into how research works and if there is a specific topic you would like us to share on, please send us an email on info@quotemonster.co.nz

Fidelity Life’s premium changes are now live!

We are pleased to confirm that the premium changes to Life, Trauma and Income Replacement covers for Fidelity Life, effective 1 June 2023, are now live on Quotemonster.

Fidelity is waiving policy fees effective 1 June to 31 August 2023 and Quotemonster also reflects this offer.

To read more on this, please click here.

Happy Crunching!

Quotemonster Information Security Bulletin – keeping safe online

This is our fifth information security bulletin, all about keeping your Quotemonster account secure and keeping safe online.

As a valued user of quotemonster.co.nz, we want to ensure that your personal information remains secure, and your privacy is safeguarded. With cyber threats becoming increasingly sophisticated, it's crucial to adopt best practices to enhance your online security. Here are some friendly reminders and recommendations to help you stay protected:

Create a strong and unique password: Make sure your password is at least eight characters long and includes a combination of uppercase and lowercase letters, numbers, and special characters. Avoid common phrases, predictable patterns, or personally identifiable information. If you have trouble remembering them, try using a password manager, such as LastPass.

Use a different password from your other accounts. Keep everything separate so that if one account is compromised your attackers do not gain access to them all.

Never use your name, username, or part of your email address as your password.

Regularly update your password: We recommend changing your password periodically, ideally every three to six months. Regularly updating your password helps protect against potential breaches and unauthorized access to your account.

Familiarise yourself with two-factor authentication (2FA) - we are glad you are all using 2FA to log onto our site. This additional layer of security significantly reduces the risk of unauthorized access by requiring a second verification step, usually through a code sent to your email or your preferred authenticator app. Ensuring you are familiar with the process means you will not be frustrated when asked for a code from your app – and you can easily find it and log on.

Do not share logins: While it may be tempting to share your login credentials with trusted individuals, it's important to remember that doing so compromises your security. Encourage each person who needs access to create their own account, ensuring accountability and preventing potential misuse.

Stay vigilant against phishing attempts: Cybercriminals often employ phishing techniques to trick individuals into revealing sensitive information. Be cautious of emails or messages requesting personal details. Avoid clicking on unfamiliar links and verify the authenticity of any communication before sharing any information.

Some notes on good general online safety:

Keep your devices and software up to date: Regularly update your operating system, web browsers, antivirus software, and other applications to ensure you have the latest security patches and features. These updates often contain critical fixes that address known system vulnerabilities. Also, having a modern computer (less than five years old) running up to date software, will greatly enhance your experience of using the site – its quicker, as well as more secure.

Be mindful of public Wi-Fi networks: When accessing our service on the go, exercise caution when using public Wi-Fi networks. Public networks may lack proper encryption, making your data vulnerable to interception. Whenever possible, connect to secure and trusted networks or use a virtual private network (VPN) for added protection.

Remember, the security of your personal information is our priority. Adopting these proactive measures will significantly contribute to safeguarding your privacy. If you ever have any questions or concerns regarding the security of our service, please don't hesitate to reach out to our support team.

Want to know more?

We are here to help! You can email us to ask for copies of past security bulletins. You can also review our outsource provider statement at the bottom right-hand corner of every page on the site at www.quotemonster.co.nz. More information about relevant certifications, policies, and procedures will be shared in future information security bulletins. We recommend you keep these with other compliance documents.

Please contact us on 09 480 6071 or at info@quotemonster.co.nz if you have any concerns or questions.

ISB 05-202305

Quality product research database upgrade

We have just uploaded QPR Database version 152 and 152a into our Dropbox folder.

This version of the database includes the following changes:

Changes made in 15.2a:

* ANZ - new policy document effective 06/03/2022

> no rating changes applied

*Revisions made to Medical Amount Scores in V15.2 for:

> Fertility benefit

> Non-surgical benefit

> Oral surgergy benefit

> Overseas treatment

> Physiotherapy

> Pregnancy

> Treatment in Australia

> Surgical benefit

> Recovery benefit

> Minor surgery benefit

Changes made in 15.2:

* Correction made to version summary log (V15.1 released 31-Jan-23) - note should read:

> FSR for PL/BNZ life update from A- to A

* Cigna rebrand to Chubb Life effective 06/03/2023 - no rating changes applied

* Kiwibank rebrand to nib effective 01/06/2023

* MAS - new policy document update for Life & IP effective 01/12/2021

* Business rating for AIA, Asteron, Fidelity, Chubb & Partners:

> TPD

* Specific Injury rating for AIA, Asteron, Chubb & Partners

> Package weighting updated to reflect the addition of SI

* Reviews:

> Medical:

* Exclusions updated for NIB, SX and PL

> IP:

* Insurable Income - rating added for Westpac

* Inflation Adjustment - rating removed for ANZ

> Trauma:

* Instant Buyback for PL Immediate Trauma and Asteron Continuous Trauma

* Heart attack sub item remediation for nib

> TPD:

* Benefit Definition over 65

For advisers the best way to explore the changes is to produce a research report on quotemonster. For product managers please refer to the change logs on the revised database that has been sent to you. For more information please contact one of the research staff.

Quality Product Research: Research Advisory Board – Central Representatives

A big welcome to the Central Representatives of our Research Advisory Board, we are honoured to have you on board!

From top left: Tony Dench (independent chair), Louise Grinstead (board member), Doreen Dutt (QPR representative), Russell Hutchinson (QPR representative)

From bottom left: David Jobson (insurer representative – Partners Life), Samuel Rees-Thomas (board member), Joshua Logan (board member)

Our board met in Wellington in the beginning of May with three topics for discussion:

The proposed rating of Business lump sum products – at the time, we prepared draft ratings for Life and TPD and received highly valuable feedback from our members allowing us to modify and progress this project.

Review of Trauma Incidence – our ‘incidence’ feature is vital to Trauma Research and with the help of claims data from Gen Re, we reviewed our current incidence, however, will be proceeding with an external consultation before these are updated on Quotemonster.

Legacy and recently closed products – we were interested in an adviser’s perspective on if and how these products should be presented on Quotemonster.

The feedback from our Research Advisory Board meetings has prompted us to create infographics that we believe will strengthen the advice you provide to your client, and we are excited to be able to feature them in our upcoming Roadshow.

For more information on our Research Advisory board please click here.