Chatswood serves the life and health insurance sector in New Zealand with market intelligence, data, and bespoke consulting services. Some of these are provided in conjunction with Quality Product Research Limited - a subsidiary that brings you Quotemonster.

We believe that good decisions are more likely to occur when we have good information about the market environment in which we operate. Intuitive leaps and creative decisions are always required, of course, but the more they are based on a firm foundation of observation, the better they tend to be.

Lifetime group acquires an advisory firm specialising in employee benefits

The Lifetime Group, a Christchurch-based, full-service financial advisory firm, has bought Protection Solutions, which specialises in employee benefits schemes.

The undisclosed transaction price includes cash and shares, with Grant Uridge and Thurl Gibbs of Protection Solutions both taking a 4.5% stake in Lifetime.

The merger expands Lifetime’s capabilities in personal and business insurance advice, with Protection Solutions currently having 13 group schemes on its books.

More daily news:

The Adviser Platform (TAP) is offering a 50% discount for six months

AM Best will be holding its Insurance Market Briefing – Auckland on November 16

ASB receive the 2023 Make it Easy Award for their Easy English guides

FSC request members participate in their member satisfaction survey

ANZ named Canstar's 2023 Bank of the Year in the Agribusiness category

Covid-19 cases spike across the country, possible we are at the start of a new wave

Industry-relevant changes as new government is ushered in

With Labour soon to hand over control to a National and ACT led government (perhaps with support from NZ First), the question on everyone’s lips is what does this mean for our sector?

National have previously come out against the proposed Income Insurance Scheme, with Christopher Luxon calling the levies required to fund the scheme a ‘job tax’. One of National’s 100 day action plan pledges is to stop work on the so-called ‘job tax’. This change could be seen as a positive move as last year Risk Info NZ ran a poll with 80% of respondents not supporting the introduction of a state-backed income insurance scheme.

National promised to repeal the Conduct of Financial Institutions Act (CoFI), due to come into force in March 2025, which they’ve said “makes credit more expensive and harder to obtain even for basic services such as overdrafts and mortgages”. Meanwhile, Katrina Shanks, chief executive of Financial Advice NZ, has said it would be ‘preferable’ to tweak CoFI, rather than scrap it altogether, as the industry is very supportive of legislation that endorses good conduct and culture within the sector.

National has promised to roll back measures brought in by Labour including the Credit Contracts and Consumer Finance Act (CCCFA), with their rebuilding the economy plan saying they will “Cut financial red tape that is stifling investment, including significantly reducing the scope of the CCCFA which has restricted access to credit.”

National has said they will allow people to split their KiwiSaver between multiple providers, which they say will ‘drive innovation, boost competition and put downward pressure on fees’, though industry players have reservations around the complexity and added costs of doing this. Another tweak to the KiwiSaver scheme they have promised is allowing young people to use their retirement savings to pay a rental bond. Instead of tinkering with the scheme, the FSC is instead calling for a comprehensive review of KiwiSaver settings.

One of the agenda items on National’s 100 day action plan is to remove the Reserve Bank’s dual mandate (of managing inflation and supporting maximum sustainable employment) to get the RBNZ purely focused on getting inflation down to targeted levels.

From a health perspective, National’s 100 day action plan includes extending free breast cancer screening for women aged up to 74, from the current cutoff of 69 years of age. National have said they will allocate $280 million in ring-fenced funding to PHARMAC over four years to pay for 13 cancer treatments not currently funded in NZ. National have said they will deliver faster access to mental health services through their Mental Health Innovation Fund, which will initially see up to $20 million in matching funds distributed to community mental health organisations who are delivering strong results for Kiwis in need. They have pledged to extend free postnatal stays for mothers of newborn babies to three days and provide free continuous glucose monitors to type 1 diabetics aged under 18.

National’s five major targets for health will be:

· Shorter stays in emergency department – 95% of patients to be admitted, discharged or transferred from an emergency department within six hours.

· Faster cancer treatment – 85% of patients to receive cancer management within 31 days of the decision to treat.

· Improved immunisation – 95% of two-year-olds receiving their full age-appropriate immunisations.

· Shorter wait times for first specialist assessment – a meaningful reduction in the number of people waiting more than four months to see a specialist (target to be set in government).

· Shorter wait times for surgery – a meaningful reduction in the number of people waiting more than four months for surgery (target to be set in government).

To attract and retain more healthcare workers they have said they will incentivise more people to study nursing and midwifery with a bonding scheme that will pay their student loan for five years if they commit to working in New Zealand. They have said they will establish a relocation support scheme, offering up to 1000 qualified overseas nurses and midwives relocation grants worth up to $10,000 each to support their move to New Zealand. National have pledged to establish a third medical school at the University of Waikato, with satellite training centres in regional areas. They’ve also said they will increase the number of medical school placements at Auckland and Otago by a total of 50 per annum from 2025.

We will be closely following these proposals and will report back as and when things change.

More daily news:

Chubb Life underwriting masterclass 24 October

FMA publishes latest 'Money with Mary' about investing more ethically

NZ's annual inflation rate dropped to 5.6% in September, from 6.0% in June

More people worldwide are now dying of non-melanoma skin cancer than melanoma

PWC summarise changes outlined by the CoFI regime

PWC have produced a useful summary of the key changes outlined by Financial Markets (Conduct of Financial Institutions) Amendment Act (CoFI), which was passed on 29 June 2022. License applications opened in July this year and CoFI will come into force in March 2025. The Ministry of Business, Innovation and Employment (MBIE) is working on regulations to support the CoFI regime, which are expected to be released later this year.

In short, the key aspects of the CoFI regime are:

· Promoting good conduct and culture.

· Complying with a set of duties and obligations that help protect customers and promote good conduct.

· Financial institutions need to be licensed by the Financial Markets Authority (FMA) to operate in New Zealand.

· The FMA has increase supervisory and enforcement powers.

· A focus on delivering good outcomes for customers.

Penalties for breaches of CoFI’s regulatory requirements include:

· The FMA taking enforcement action which could include imposing fines, giving directs to take corrective action or taking the institution in breach to court.

· Maximum penalties of $5 million for companies and $500,000 for individuals.

· The FMA could order compensation for customers.

· The FMA could suspend or cancel the licence of a financial institution.

· Reputational damage.

PWC set out a helpful guide of activities you can do now and in future to prepare for COFI. The FMA has information on Fair Conduct Programmes and more detailed information on CoFI, including how to apply for a financial institution licence here.

More daily news:

Sharron Botica shared what's behind AIA's Digital Agency functionality

Stimulating your brain can increase your resilience against developing dementia

How intermediaries can prepare for CoFI

MinterEllisonRuddWatts has published an article on how intermediaries can prepare for CoFI.

They define who qualifies as an intermediary and a consumer; outline insurers’ obligations in setting up and maintaining a fair conduct programme; outline what intermediaries can expect financial institutions to ask them for when assessing distribution methods; give examples of what contractual agreements should contain in terms of expectations, commissions, assurances and how to remedy deficiencies; highlight the need to review internal policies.

They make the point that intermediaries which are FAPs warrant a lower level of controls in relation to their distribution arrangements, as they are already regulated and pose a lower level of risk.

If you’re still getting your head around CoFI obligations, we recommend you check it out.

More daily news:

Grant Robertson reconfirms that the NZIIS is still on hold

Registrations open for Financial Advice NZ’s Thrive 2024 Annual Conference 5 – 6 March

Voting for Financial Advice NZ Board Member Director (Risk) is open

Katrina Shanks writes about teaching children financial literacy

Partners Life ‘new adviser’ online training course starts 16 October

Oncologists write an open letter to Pharmac, advocating for newer and better-funded medication

Southern Cross responds to accusations it dropped a $60k benefit without informing customers or advisers

Southern Cross has refuted a Good Returns article where advisers complained about not being informed about Southern Cross dropping a $60,000 a year benefit for non-surgical hospitalisations.

Southern Cross removed the non-surgical hospitalisation benefit as part of the Society’s benefit review in 2020, and Southern Cross’ head of customer strategy and experience, Nic Johnson has said that “Members were communicated with at the time of the benefit change.”

Johnson said that Southern Cross advisers were informed of the changes at the time via a virtual meeting, and that the company’s adviser gateway portal to manage their customers’ policies had information on the changes also.

Johnson said

“The original intention of the non-surgical hospitalisation benefit was as a 'catch-all' for eligible healthcare services that required in-hospital medical treatment. Based on a 2019 review of our claims data, which showed that the benefit was not widely utilised, it was assessed that this benefit was no longer fit-for-purpose.”

“The majority of medical (or hospitalisation) claims at the time were already covered under existing benefits, such as the surgical procedures, chemotherapy, radiotherapy and diagnostic tests/imaging benefits.”

We have commented on the change here.

Quality Product Research are in the process of conducting a review of the score for the feature, giving Southern Cross time to respond with more details of equivalent benefits being present in other parts of the medical insurance. We will raise the results of the review with our Southern Research Advisory Board next month – and update research subscribers immediately.

More daily news:

Katrina Shanks writes about whether cryptocurrencies are a safe investment

Rob Hennin talks about why he loves working in the insurance sector

Southern Cross funds the ‘Under One Umbrella’ report on mental health and addictions

nib publishes their top five medical claims for July

Q&A with Akira Yamashita and Satoshi Shimasaki from Partners Life

We’ve had the pleasure of talking to Akira Yamashita, Deputy Chief Executive Officer and Satoshi Shimasaki, Deputy Chief of Finance who were both integral to the sale of Partners Life to Dai-ichi Life Holdings, Inc.

Q&A with Akira Yamashita Partners Life Deputy Chief Executive Officer

Could you outline the path your career has taken?

I joined Dai-ichi Life over 25 years ago. I have worked in various companies and countries but I have always worked for the Dai-ichi Life group. My career started in the sales branch office where I was part of the sales promotion team for 3 years. This is where I learned the basics of insurance sales activity. For the next 5 years, I worked as an economist. I forecasted the upcoming economic conditions and researched and analysed certain economic topics. This gave me good experience and the skill set to understand macro-economic insights which is still useful for me when considering various strategies.

In the last 20 years, I’ve been engaged in overseas (from Japan) business. This started from New York for 3 years as corporate administrator, Mumbai (India) for 4 years as the head of financial planning & budget control, Sydney (Australia) for 4 years as manager of the Finance team to support the implementation of strategic initiatives and development of a sound business plan. I also spent time in the head office in Tokyo working on the preparation and implementation of further global governance structure development. In addition, I established an intermediate holding company to create strategic proposals for both the business and talent strategies.

Now I am here in Auckland as Deputy CEO of Partners Life, to bridge the various interactions/relationships between shareholder “Dai-ichi Life Holdings” and Partners Life.

What attracted you to the insurance industry?

I want to spend my working days feeling fulfilled from being engaged with helping people. There are many jobs that can provide this, but I believe more in the business that can provide support in a timely manner when people are struggling or need help. What I like about the Life Insurance industry is that people’s lives might move along with nothing to worry about, but life insurance comes into play when they suffer financially if the person responsible for the household income and expenses has fallen ill or died. Also, these days I’ve found that “health and wellbeing” initiatives are an attractive addition by industry players.

Tell us about your time at Partners Life so far.

It has been almost half a year since I joined Partners Life. I still feel fresh to this organisation and excited to catch up and try new things. The operating and management style of the company is very efficient and effective overall, and this could be worth sharing with our Dai-ichi group companies.

How would you describe the culture at Partners Life?

The decisions we make are always based on “Do the right thing”, which is one of our corporate values. People in Partners Life use their energy to help provide the appropriate outcome to our client, rather than just aiming for our company growth. There is no strong hierarchy but a flat open forum to discuss and decide things, and I see this as a strength of this organisation.

What is one thing you wish someone had told you when you were younger?

No one had told me how much our daily lives would be driven by technology, such as online transactions, and AI coming in to play. I would have been grateful if someone had told me to study science when I was considering my major in university.

Q&A with Satoshi Shimasaki Partners Life Deputy Chief of Finance

Could give us an overview of your career to date?

I’m currently working for the Post Merger Integration at Partners Life, as a liaison officer. Before joining Partners Life, I was the head of M&A at Dai-ichi Life Holdings, responsible for strategic planning and executing M&A in overseas business.

I started my career in international legal practice. After experiencing an internship program at Prudential Financial (US), where I learned the US life and annuity operation, I joined the Planning and M&A team at Dai-ichi HQ. As a core member of the transaction team, I helped achieve multiple deals. My role in the early days was legal/documentation and negotiation, then I gradually expanded my playing field to accounting, finance, and finally, entire project management. I was one of the three negotiation members of Dai-ichi’s iconic M&A in the US back in 2014, and after completing that I spent three years with the M&A team of the US subsidiary. I have a strong connection with the Australian subsidiary’s transaction team, with whom I accomplished two joint M&As in Australia recently. I graduated magna cum laude from Columbia Business School in 2017.

What attracted you to the insurance industry?

While I was at university, the insurance industry seemed to be complicated and this stimulated my passion.

Tell us about your time at Partners Life so far.

Since day one, I’ve been enjoying working with my amazing colleagues. Personally, I love being in Takapuna, which is far different from where I came from (Tokyo & New York).

How would you describe the culture at Partners Life?

Always restless and generous by nature, as shown in the company values. It is like a Cessna plane with a jumbo jet engine.

What is one thing you wish someone had told you when you were younger?

Make a side trip on the way. Don’t rush. Detours sometimes make your life better.

More daily news:

Complaints to FSCL rose by 25% to 1,349 in the year to 30 June 2023

Voice deepfakes are the latest scammers trick

FSC Young people and the cost of living crisis research launch 28 September

Microinsurance continues to grow globally

Centrix finds Buy now, pay later is the most common first debt product among people under 25

Highlights from nib’s 2023 Community Report

nib has released their 2023 Community Report, highlighting community initiatives across New Zealand and Australia delivered by nib, the nib foundation and employee volunteering and fundraising. The nib foundation is nib’s charitable organisation that focuses on helping people and communities live healthier lives. Some of the highlights include:

As part of the nib foundation’s Prevention Partnerships program, that aims to tackle risky behaviour, nib launched the Clearhead Finding Purpose tool in NZ.

Nib donated $20,000 to KiwiHarvest to distribute food relief to those affected by the Auckland floods and Cyclone Gabrielle. KiwiHarvest donated 57,000 portions of fresh produce.

Members, employees and the public voted for which local charity partner should receive a share of $30,000 as part of celebrating nib NZ’s 10th birthday – Ronald McDonald House received $15,000, KiwiHarvest received $10,000 and Clearhead received $5,000.

More than 8,500 members used Clearhead’s Finding Purpose tool.

Glen Eden Intermediate won a $10,000 cheque from the nib Little Legends $10k relay for their junior rugby team.

nib were the naming rights sponsor for nib IronMāori TOA, 17-hour event that includes a 3.8km ocean swim, 180km cycle and 42.2 km run.

nib were the naming rights sponsor of the nib Blues wāhine team and they donated $11,500 worth of specialist recovery equipment to the team.

Shannon Leota and Katelyn Vaha’akolo were each the recipients of a $5,000 nib Blues Health & Wellbeing Scholarship.

nib partnered with Save the Children, to help families in Ukraine gain access to essentials, such as, food, clean water and basic hygiene supplies; as well as cash grants, emergency services and mental health support.

Removed weeds and rescued trees with Conservation Volunteers New Zealand at Papakura stream and Sanders Reserve.

Nib staff collected and delivered Christmas presents to those in need with The Blues and the Salvation Army.

Packaged around 3,500kgs of food to deliver to local community kitchens and people in need across Auckland.

Overall across NZ and Australia, nib group delivered $6.6 million in community funding and over 1,500 volunteer hours.

More daily news:

‘5 mins with FMA’ podcast #7: Phony investment scams and how to protect yourself

FSC Trans Tasman Strategic Leaders Summit 5 - 7 March, Auckland

FSC webinar 'How’s the mental health of your network?' 19 September

Melanie Gorham believes level-5 has shrunk the NZ insurance broking talent pool

FMA has four strategic priorities over the next year

Katrina Shanks talks about what an organisations online presence has in common with quality advice

Kiwibank is rolling out a financial wellbeing programme for its staff

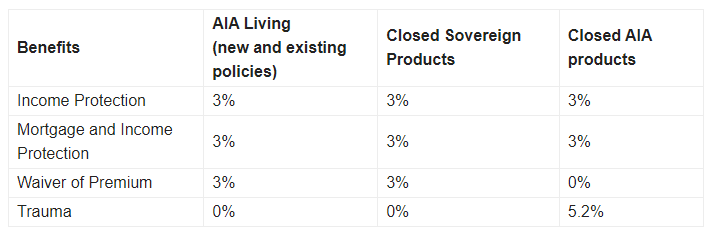

Premium increases at AIA

AIA is increasing premiums on its income protection (IP), waiver of premium and closed trauma products. AIA have said the increases are based on a gradual increase in IP claims and a higher level of claims on closed AIA trauma products compared with their wider trauma portfolio.

The table below shows the pricing increases, with closed AIA trauma products set to have staggered price increases at a rate of 5.2% a year over the next three years.

More daily news:

Tony Vidler recommends advisers keep client consultations simple

The IMF says the NZ Government needs to trim spending or risk prolonging high inflation

Banking ombudsman recommends changes to loan application processes

MyLifeMatters campaign calls for new medicines and more Pharmac investment

Political parties announce policies requiring financial literacy to be taught in schools

Labour has announced a financial skills in schools policy that would require financial literacy to be taught at all levels in all schools by 2025, if Labour are re-elected.

Labour leader and Prime Minister Chris Hipkins said

“We know that our young people, to set them up for success, we need to make sure they understand the basics of budgeting, they need to understand basic financial concepts, they need to understand how to be good with money, they need to understand things like interest rates, KiwiSaver, insurance, debt, borrowing."

"We want to make sure they’re learning those core skills while they are at school, because we know that that's going to set them up well for a prosperous life beyond school.”

National Party deputy Leader Nicola Willis has said that, if elected, a National-led government would also make financial literacy compulsory in schools.

With both major parties backing the proposal, it is likely to become Government policy, regardless of the results of the election.

We share a view that poor financial literacy is a problem – as many acknowledge. Yet it is not clear to us how successful schools can be in addressing the issue. One is that skills taught in school tend not to be retained unless they are something that children have a particular interest in. Understanding prices, money, borrowing and saving, are likely to be useful at an earlier stage, for example, than insurance and home loans. As with all curriculum changes, making it relevant and balancing it against other educational needs is something that requires careful consideration.

Southern Cross release their Workplace Wellness Report 2023

Southern Cross have released their Workplace Wellness Report 2023, an in-depth analysis of health and wellbeing in the workplace. Southern Cross surveyed 137 enterprises across New Zealand, representing 135,742 employees, or 6.5% of all NZ employees.

Some of the key findings include

• The average rate of absence per employee was 5.5 days, the highest ever. It was also the first full calendar year since the increased sick leave entitlement of 10 days per annum was in force and there was a mandatory stand-down of seven days for people who contracted Covid-19 that was in place during the time of the survey. From 2012 – 2020 the average ranged from 4.2 to 4.7 days per year.

• The cost to an employer for a typical employee’s absence is now $1,235 annually. Over the entire economy, the cost of absence reached approximately $2.86 billion, due to both increased absence rates and rising labour costs. This is a significant increase from the $1.85 billion cost for the total economy in 2020.

• 49.7% of organisations have observed an increase in stress in 2022. Workload is the main cause of work-related stress/anxiety and long hours as the second main cause of stress. Given the tight labour market conditions, it’s unsurprising that job uncertainty/redundancies dropped down the rankings significantly this year. Financial concerns are now the number one non-work-related stressor.

• 22% of organisations have reported instances of ‘quiet quitting’, where employees signal their intention to work within defined work hours only.

• The impact of staff wellness on productivity has grown to a mean of 4.33 out of 5, up from 3.91 in 2020.

• The main practices businesses are using to identify mental wellbeing/stress are staff surveys and training for managers.

• The top six benefits provided to improve employee well being were: an Employee Assistance Programme (EAP); vaccinations; flexible hours/working at home; education/training; wellbeing programmes; and parental leave.

• Almost 40% of organisations provided some form of subsidised health insurance for at least some employees. For employers who do not provide health insurance for employees, cost is a major barrier, with 53.4% of organisations saying a decrease in the cost of health insurance would prompt them to consider providing health insurance as a benefit. 31.9% would consider providing health insurance if they had evidence that it assists in retaining staff due to its perceived value. 14.7% would consider providing health insurance if they were approached by a health insurer to discuss the fundamentals of insurance, policies, benefits and wellness programmes.

• More than half of organisations allow more people to work from home since 2021, with one to two days per week as the most common working from home option.

• All organisations who had made changes around allowing staff to work from home or remotely saw it as a positive move, with employees happier to have more flexibility. On the flip side, almost all large organisations and about half of smaller organisations reported some employees felling isolated, some issues around collaboration.

More daily news:

Katrina Shanks writes about how the cost of living crisis is affecting middle income earners

Andrew Bayly says CoFi needs to go

Chubb Life are holding a marketing masterclass on 30 August

mySolutions webinar 'Lend and Protect' 9am 30 August

The Government’s mental health and addiction programme has hit one million support sessions

Research finds 55% of kiwis are struggling with their financial situation