Chatswood serves the life and health insurance sector in New Zealand with market intelligence, data, and bespoke consulting services. Some of these are provided in conjunction with Quality Product Research Limited - a subsidiary that brings you Quotemonster.

We believe that good decisions are more likely to occur when we have good information about the market environment in which we operate. Intuitive leaps and creative decisions are always required, of course, but the more they are based on a firm foundation of observation, the better they tend to be.

Government has repealed parts of the Credit Contracts and Consumer Finance Act

The government has repealed some parts of the Credit Contracts and Consumer Finance Act (CCCFA). Commerce Minister Andrew Bayly said of the affordability regulations introduced to the CCCFA in December 2021

“These regulations created unnecessary compliance costs and are an excessive barrier for lending. And worse, the regulations failed to protect the most vulnerable Kiwis – the very people they were intended to safeguard”

The time to process loans increased substantially, with Minister Bayly saying some lenders had told him small loans that used to take two hours to process took up to eight hours to process under the new regulations.

Additional reforms to the act include:

Improving dispute resolution to better protect consumers.

Exempting councils from the CCCFA so they are able to offer low-risk financial products to help households improve their energy efficiency by installing heat pumps and insulation.

Removing duplicate reporting requirements.

We hope that the relaxation on small loans flows through to banks being able to offer more flexibility to people with what amounts to a timing issue, rather than a lending issue. But we know that lending rules are notoriously difficult to manage. This is one of the reasons why aspects of the wider programme are of more interest.

Minter Ellison puts the changes into context within a program of changes to financial law and regulation which the government has planned.

Of particular interest are the changes in supervisions structures with the responsibility for administering the CCCFA moving from the Commerce Commission to the Financial Markets Authority. Lending is a financial product, and we think the Financial Markets Authority, with conduct supervision responsibilities and, essentially, all the other financial products, is probably a good home for this law from an ongoing regulation perspective.

More daily news:

Jon-Paul Hale highlights issues with digital documents

The Ombudsmen FSCL and the IFSO Scheme are in merger talks

Empower Women breakfast at the National Strategy for Financial Capability Partners Conference

Andrew Dentice urges more discussion on the benefits of open banking

Pharmac outlines funding plans for continuous glucose monitors for type 1 diabetics

UniMed gets approval from RBNZ to take on Accuro’s portfolio

UniMed has received approval from the Reserve Bank of New Zealand to take on the portfolio of insurance co-operative Accuro.

Once Accuro’s 30,000 members have been transferred to UniMed, UniMed will be the third largest health insurance provider in New Zealand, with combined membership of 140,000.

Once the transfer is finalised, members will transition to being part of the UniMed society, though the Accuro brand will remain. Accuro members will continue to have the same policies and healthcare benefits as they do now. Once the transer is complete Accuro will cancel its insurance licence and take steps to dissolve the Accuro Health Insurance Society.

UniMed Chair Peter Tynan says

“The additional scale will ensure UniMed is in the best possible position to create efficiencies, develop new services and products and meet the challenges of increasing member expectations all at a time when the cost of health services is rising, and the regulatory environment continues to evolve.”

More daily news:

The FSC publish their Regulatory Outlook for April

nib would welcome Medicines Act review and regulation to get more treatment options approved

AIA launch 2024 CEO Think Tank programme

AIA offer one month's premium free on new eligible policies issued by 17 June 2024

The New Zealand Society of Actuaries appoints Helen Mexted as chief executive

Fidelity Life report digs into the role of financial advice in New Zealand

Fidelity Life’s ‘Advice for good: Rethinking New Zealand’s relationship with financial advice’ report highlights some worrying findings in New Zealander’s feelings towards their financial situation.

Fidelity Life’s ‘Advice for good: Rethinking New Zealand’s relationship with financial advice’ report highlights some worrying findings in New Zealander’s feelings towards their financial situation. The report found that:

28% of kiwis feel their financial situation is out of their control.

47% of kiwis often or always worry about money, and 53% of under-35s saying they always worry about money.

The majority of New Zealanders don’t feel confident making financial decisions until after age 55 – once this age is reached 63% feel confident in their money decisions.

Only 28% of women feel confident about their financial outlook, compared to 44% of men.

While 88% of kiwis agree financial advisers are the most trustworthy source of financial information, only 22% have consulted one – though 36% have sought help from family.

Many New Zealanders don’t know where to get trusted financial advice, with 41% of those under-35 unable to say where to find good advice.

There are different emotions towards money depending on ethnicity, with 30% of Māori and 38% of Middle Eastern, Latin American and African (MELAA) respondents said their financial situation made them feel overwhelmed. Meanwhile, 27% of Pacific Islanders were ashamed, and 58% viewed their financial situation negatively overall. 74% of Pacific Islanders, 59% of Asians and 56% of Māori respondents feel unconfident or unsure making financial decisions.

There was some good news about New Zealanders’ finances too.

88% of New Zealanders feel like they typically have enough to pay the bills.

34% feel financially comfortable, especially older New Zealanders – with 81% of those aged 65+ feeling positive about their financial situation.

Attitudes towards the future seem to be optimistic, with 41% feeling their financial situation will improve in the next 12 months, compared to 28% expecting things to worsen.

Kiwis are generally focusing on short-term horizons, with 89% of people prioritising day to day spending, 65% focusing on saving and 57% concentrating on paying off debt. Only 13% put growing their wealth and 4% put protecting their finances as their highest priority. 34% of those surveyed didn’t have any form of insurance and only 11% had consulted an insurance adviser.

This short-term focus is highlighted again with only 3% of those under 35 mentioning setting themselves up for a comfortable retirement as an aspiration, with home ownership being the number one goal in this age bracket. While retirement seems a long way away when young, only 23% of those in the 55+ age group mentioned a comfortable retirement as one of their aspirations, despite being less than a decade away from receiving the pension. 79% of those surveyed had KiwiSaver, 30% have stocks and shares and 17% have managed funds.

There seems to be a lack of understanding of the benefits financial advice can bring to people at all ages and stages of life. 31% of respondents said they don’t see the relevance of professional advice, and 10% listed being embarrassed or scared or consider their financial position to be private as a barrier to seeking advice. Only 5% of people stated they don’t know how to/who to talk to as a reason. Part of the lack of understanding on the benefits on advice might be due to a lack of familiarity on the role advisers perform, with only 13% being able to describe it with any confidence. Borrowing money was the most common catalyst for seeking out advice (48%) compared to 36% looking to invest to grow wealth. Just 28% have sought advice on products like income protection insurance or mortgage insurance. For those who consulted a professional financial adviser, 81% said getting financial advice provided peace of mind and 70% said it helped them achieve their goals.

Campbell Mitchell, Chief Executive of Fidelity Life said

“…the evidence shows most New Zealanders aren’t seeking financial help, either through regular financial health checks or at key life stages, until they’re nearing retirement – when it may be too late,”

“As a result of seeking amateur advice, we get stuck in the same old ways of doing things and can’t see a way forward – especially when the people we most often turn to for advice, our parents, have experienced different conditions. Baby Boomers who have achieved financial success via the traditional route of buying a home and an investment property may consider themselves financially savvy without taking into account the fact they’ve lived through one of the greatest property booms in our history, and that as the world changes, a different approach might work better today”.

The report was commissioned to explore attitudes towards financial advice and how to overcome the barriers to seeking professional guidance. The report surveyed more than 1,100 New Zealander’s aged 18 – 69, representative across age, gender, ethnicity and income level and consisted of a mix of quantitative and qualitative interviews.

More daily news:

mySolutions webinar 9am 6 March 'Lessons and experiences from FMA monitoring visit'

Survey finds NZers want stricter penalties for companies suffering cyber breaches

Nick Astwick explains how Southern Cross Health Society remains economically sustainable

Nick Astwick, chief executive at Southern Cross, has spoken about how Southern Cross Health Society remains economically sustainable. He details the three key things that the not-for-profit friendly society relies on to keep it sustainable.

Nick Astwick, chief executive at Southern Cross, has spoken about how Southern Cross Health Society remains economically sustainable. He details the three key things that the not-for-profit friendly society relies on to keep it sustainable:

· Young and healthy members - Astwick talks about how having younger, healthier members keeps claims down.

· Prevention – a focus on preventing sickness from happening, like a pilot programme the Health Society is running that offers bowel cancer screening.

· Membership growth and retention – ensuring affordable coverage and accessible benefits to help maintain tenure.

More daily news:

Swiss Re release report on the global economic and insurance market

Partners Life "Last Performance” campaign wins at Agency of the Year awards

The FSC welcome the incoming government

Southern Cross Health Society Annual General Meeting 6 December

Asteron Life customers can score a $50 Prezzy card for every $500 in new premium, up to $5000

MAS webinar 'Financial wisdom for a purposeful retirement' 5 December

Sharesies has launched its KiwiSaver scheme to the general public

David Green says mortgage lending should be taken out of the CCCFA and given its own legislation

Chubb has appointed Adit Witjaksono as property manager for Australia and New Zealand

FintechNZ Annual Meeting 2023 rescheduled to 6 December

Industry-relevant changes as new government is ushered in

With Labour soon to hand over control to a National and ACT led government (perhaps with support from NZ First), the question on everyone’s lips is what does this mean for our sector?

National have previously come out against the proposed Income Insurance Scheme, with Christopher Luxon calling the levies required to fund the scheme a ‘job tax’. One of National’s 100 day action plan pledges is to stop work on the so-called ‘job tax’. This change could be seen as a positive move as last year Risk Info NZ ran a poll with 80% of respondents not supporting the introduction of a state-backed income insurance scheme.

National promised to repeal the Conduct of Financial Institutions Act (CoFI), due to come into force in March 2025, which they’ve said “makes credit more expensive and harder to obtain even for basic services such as overdrafts and mortgages”. Meanwhile, Katrina Shanks, chief executive of Financial Advice NZ, has said it would be ‘preferable’ to tweak CoFI, rather than scrap it altogether, as the industry is very supportive of legislation that endorses good conduct and culture within the sector.

National has promised to roll back measures brought in by Labour including the Credit Contracts and Consumer Finance Act (CCCFA), with their rebuilding the economy plan saying they will “Cut financial red tape that is stifling investment, including significantly reducing the scope of the CCCFA which has restricted access to credit.”

National has said they will allow people to split their KiwiSaver between multiple providers, which they say will ‘drive innovation, boost competition and put downward pressure on fees’, though industry players have reservations around the complexity and added costs of doing this. Another tweak to the KiwiSaver scheme they have promised is allowing young people to use their retirement savings to pay a rental bond. Instead of tinkering with the scheme, the FSC is instead calling for a comprehensive review of KiwiSaver settings.

One of the agenda items on National’s 100 day action plan is to remove the Reserve Bank’s dual mandate (of managing inflation and supporting maximum sustainable employment) to get the RBNZ purely focused on getting inflation down to targeted levels.

From a health perspective, National’s 100 day action plan includes extending free breast cancer screening for women aged up to 74, from the current cutoff of 69 years of age. National have said they will allocate $280 million in ring-fenced funding to PHARMAC over four years to pay for 13 cancer treatments not currently funded in NZ. National have said they will deliver faster access to mental health services through their Mental Health Innovation Fund, which will initially see up to $20 million in matching funds distributed to community mental health organisations who are delivering strong results for Kiwis in need. They have pledged to extend free postnatal stays for mothers of newborn babies to three days and provide free continuous glucose monitors to type 1 diabetics aged under 18.

National’s five major targets for health will be:

· Shorter stays in emergency department – 95% of patients to be admitted, discharged or transferred from an emergency department within six hours.

· Faster cancer treatment – 85% of patients to receive cancer management within 31 days of the decision to treat.

· Improved immunisation – 95% of two-year-olds receiving their full age-appropriate immunisations.

· Shorter wait times for first specialist assessment – a meaningful reduction in the number of people waiting more than four months to see a specialist (target to be set in government).

· Shorter wait times for surgery – a meaningful reduction in the number of people waiting more than four months for surgery (target to be set in government).

To attract and retain more healthcare workers they have said they will incentivise more people to study nursing and midwifery with a bonding scheme that will pay their student loan for five years if they commit to working in New Zealand. They have said they will establish a relocation support scheme, offering up to 1000 qualified overseas nurses and midwives relocation grants worth up to $10,000 each to support their move to New Zealand. National have pledged to establish a third medical school at the University of Waikato, with satellite training centres in regional areas. They’ve also said they will increase the number of medical school placements at Auckland and Otago by a total of 50 per annum from 2025.

We will be closely following these proposals and will report back as and when things change.

More daily news:

Chubb Life underwriting masterclass 24 October

FMA publishes latest 'Money with Mary' about investing more ethically

NZ's annual inflation rate dropped to 5.6% in September, from 6.0% in June

More people worldwide are now dying of non-melanoma skin cancer than melanoma

nib release 2023 sustainability, community and climate-related disclosure reports

nib Group have released their 2023 sustainability, community and climate-related disclosure reports. Some highlights from the reports include:

· 25,990 HealthChecks were undertaken by nib members.

· Employee Experience Surveys in FY23 found an overall engagement score of 81%.

· 289 staff volunteered 1,546 hours across 14 charities.

· 34 suppliers completed continuous improvement plans to manage modern slavery risk.

· The strategic procurement team has taken a proactive step toward reducing nib’s carbon footprint by introducing environmental criteria into the Request for Proposal (RFP) process.

· nib introduced a new values-based employee recognition program where all employees have the opportunity to nominate their colleagues and vote on the most extraordinary achievements.

· nib worked with Ngāti Whātua Ōrākei to facilitate the ‘Cultural Coalition’ Program (Whatua te Aho Tukurua). This six-week program teaches participants Māori language and values, encouraging employees to integrate these learnings into regular work activities and practices.

· Gender pay equity gap has reduced to 2.75%.

· 985 Kiwis visited Clearhead’s Te Reo Māori website and chatbot

nib has identified climate-related risks including:

· increased market pressure to provide community support and insurance affordability for those experiencing climate hazards;

· increased illness & comorbidity due to chronic and compounding climate change hazard;

· trauma, illness, property destruction and disruption leading to high rates of psychological distress;

· increased incidents and severity of climate hazards causing pressure on discretionary income;

· chronic and compounding climate change impacts putting pressure on health services;

· energy and emissions performance standards creating compounding capital expenditure and operational costs;

· limitations of current regulatory and pricing mechanisms to respond to climate hazards;

· risk nib won’t meet growing mandatory reporting and regulatory requirements.

nib has developed a risk-management framework to manage and mitigate its material risks, and their board and management regularly identify and analyse risks and the effectiveness of the controls in place to manage these risks.

More daily news:

FinTech NZ is asking members to fill in their 2024 New Zealand Fintech Pulsecheck Survey

mySolutions webinar 'Roles and responsibilities of Directors' 9am 18 October

Open letter to Pharmac saying the chief executive and the chairman need to step down

Financial Advice New Zealand release ‘Value of Financial Planning Consumer Research 2023’ report

Financial Advice New Zealand’s latest study on the value of financial planning has been released. The study was undertaken in February 2023 and questioned 1,001 New Zealanders over 25 years old who earned over $90,000 per annum or held over $50,000 of investable assets on the value of working with a financial planner.

Some highlights from the report include:

· 68% of clients of financial planners are highly satisfied with their wealth versus 33% of unadvised consumers.

· 9 in 10 of those who have seen a certified financial planner feel financially secure.

· 9 in 10 clients of certified financial planner say the benefits of financial planning outweigh the costs.

· Those who haven’t engaged with a financial planner report unmet financial needs, with 2 in 5 worried about enough money to live on, 1 in 3 worried about the ability to live their desired lifestyle and 1 in 3 not having a realistic plan for a comfortable retirement.

· 99% of those who have engaged a certified financial planner trust they are acting in the client’s best interest

· 100% of those who have engaged a certified financial planner are likely to continue the relationship with their financial planner.

· Clients reported the top benefits of working with a financial planner as better financial decision-making confidence; having simplify and explain financial matters; improved financial wellbeing and peace of mind; improved confidence in ability to achieve desired standard of living.

The report also has some interesting information on the different ways different generations like to engage with financial planners.

More daily news:

AIA special offer could save clients up to 31% in premiums

Partners Life is switching to email communication for customers who want it

Katrina Shanks writes of findings on the value of financial planning services

Katrina Shanks is confident she's leaving Financial Advice NZ with a good framework in place

mySolutions are holding roadshows across the country in November

Official Cash Rate remains at 5.50%

FSC calls for a comprehensive review of KiwiSaver

Nominations for Insurance Business’s annual Elite Women are open

Malcolm Mulholland laments the lack of funded medicines in NZ

Sleep regularity is important for longevity

How intermediaries can prepare for CoFI

MinterEllisonRuddWatts has published an article on how intermediaries can prepare for CoFI.

They define who qualifies as an intermediary and a consumer; outline insurers’ obligations in setting up and maintaining a fair conduct programme; outline what intermediaries can expect financial institutions to ask them for when assessing distribution methods; give examples of what contractual agreements should contain in terms of expectations, commissions, assurances and how to remedy deficiencies; highlight the need to review internal policies.

They make the point that intermediaries which are FAPs warrant a lower level of controls in relation to their distribution arrangements, as they are already regulated and pose a lower level of risk.

If you’re still getting your head around CoFI obligations, we recommend you check it out.

More daily news:

Grant Robertson reconfirms that the NZIIS is still on hold

Registrations open for Financial Advice NZ’s Thrive 2024 Annual Conference 5 – 6 March

Voting for Financial Advice NZ Board Member Director (Risk) is open

Katrina Shanks writes about teaching children financial literacy

Partners Life ‘new adviser’ online training course starts 16 October

Oncologists write an open letter to Pharmac, advocating for newer and better-funded medication

AIA has released 2022 Claims Data

AIA has released their annual claims data for 2022.

93% of all claims received were accepted.

Paid $646.4 million in claims.

Broken down this comes to $121.5 million in Health claims, $233.8 million in Life claims, $111 million in Trauma claims, $74.4 million in Income Protection claims and $15.3 million in Total Permanent Disablement claims paid.

Over 30,000 health claims were submitted online via the myAIA customer self-service portal.

Life insurance accounted for 42% of all claims.

For those aged 20 - 29 accidents are the main claim for life cover while the main claim for life cover in those aged 30 - 59 is cancer.

Over 815,000 New Zealanders are covered by AIA.

More daily news:

AIA announces major expansion of its gym network

Jon-Paul Hale questions fairness of AIA moving policies after a couple separates

Study finds good financial advice could add almost 6 per cent to New Zealanders’ wealth in 2023

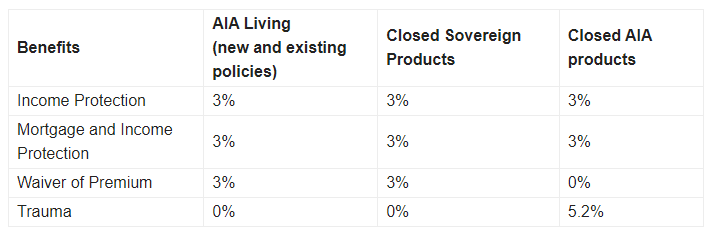

Premium increases at AIA

AIA is increasing premiums on its income protection (IP), waiver of premium and closed trauma products. AIA have said the increases are based on a gradual increase in IP claims and a higher level of claims on closed AIA trauma products compared with their wider trauma portfolio.

The table below shows the pricing increases, with closed AIA trauma products set to have staggered price increases at a rate of 5.2% a year over the next three years.

More daily news:

Tony Vidler recommends advisers keep client consultations simple

The IMF says the NZ Government needs to trim spending or risk prolonging high inflation

Banking ombudsman recommends changes to loan application processes

MyLifeMatters campaign calls for new medicines and more Pharmac investment