Chatswood serves the life and health insurance sector in New Zealand with market intelligence, data, and bespoke consulting services. Some of these are provided in conjunction with Quality Product Research Limited - a subsidiary that brings you Quotemonster.

We believe that good decisions are more likely to occur when we have good information about the market environment in which we operate. Intuitive leaps and creative decisions are always required, of course, but the more they are based on a firm foundation of observation, the better they tend to be.

AI and Machine Learning are driving benefits and reducing headcount in the insurance sector

A survey of insurers by Rackspace has found that the implementation of Artificial Intelligence (AI) and machine learning (ML) technologies are driving benefits and enabling the reduction of headcounts.

A survey of insurers by Rackspace has found that the implementation of Artificial Intelligence (AI) and machine learning (ML) technologies are driving benefits and enabling the reduction of headcounts.

The survey found over the past 12 months 62% of insurers had cut staff numbers due to the implementation of AI and ML. They found that the new technology enabled low-level analyst work to be completed by AI and ML. 52% of respondents said they had already realised substantial benefits from AI/ML, with a further 23% seeing modest benefits. 25% of respondents said it was too early to tell.

The benefits insurers listed from implementing AI/ML were

81% risk reduction, increased understanding of business/customers

79% increased sales

77% personalised marketing

75% increased productivity

73% increased revenue streams, operation cost reduction

69% improved customer satisfaction

67% faster time to profitability, reduced cost of new product development, ability to hire/recruit new talent

65% increased innovation

There are still some issues with AI, with 42% only ‘slightly trusting’ AI/ML results compared to 28% ‘strongly trusting’ results.

Talent and skill shortages were seen by 67% as the greatest challenge to further adoption of the technology; however 90% of insurers had grown their AI and ML workforce in the past 12 months.

Although this survey lumps AI and ML together there are some fundamental differences. Machine learning can be disconnected from the large volumes of training data that are used in generative AI such as Chat GPT. Although that may sound like a disadvantage, narrower pools of training data can make results from machine learning applications much more accurate for highly specific tasks. It also means that data does not have to be shared with generative AI engines – its can remain in confidential silos within the business.

ChatGPT recently put forward it’s arguments for how it can positively impact the insurance industry. While there are still plenty of cons to using ChatGPT right now, ranging from inbuilt biases and prejudices to its failure to comprehend nuance such as sarcasm, some insurance executives believe the underlying technology could be used as a starting point to build on and to jumpstart innovations in the sector.

At Quality Product Research Limited we agree that there are some great opportunities for implementation of AI and ML initiatives. With more than 15 million quotes and over 1.25million data points of data in our research databases we are well positioned to employ these tools to greater effect over the coming years.

Q&A with Karty Mayne from Rosewill Consulting

We had the pleasure of talking to Karty Mayne, Director and Compliance Consultant at Rosewill consulting.

We had the pleasure of talking to Karty Mayne, Director and Compliance Consultant at Rosewill consulting.

What services does Rosewill Consulting provide?

Rosewill Consulting was set up with a mission to make compliance sexy! If we don’t think it is who will!

We provide Licensing and Compliance Services for financial services businesses. We also conduct independent audits and compliance reviews and provide specialist training. We have an online compliance and training system that has an extensive library of up-to-date professional development material.

What do you see as areas of focus in 2024?

Here are my top three…

Newly licensed entities, such as Financial Advice Providers, Head Groups and other types of licensees will need to have a strong focus on implementation. Being regulated requires creating a workplan and delivering on it. Initial policies and procedures may have design flaws or not be sufficiently robust so this is an important time to make those key adjustments.

On a wider scale, the world is facing ongoing increases in the nature and volume of cyber-attacks. Regulators such as the FMA have published a lot of guidance on this but from our experience regulated entities still need a lot of help in this area.

The pace of regulatory change hasn’t slowed up at all. 2024 will introduce new obligations such as additional AML/CFT Regulation, Conduct Licensing, Deposit Takers Act and the review of the Insurance contract law to name a few. Plus, the Coalition government will surely be adding to this list.

Can you tell us a little bit about yourself and why you decided to start up Rosewill Consulting?

I was initially sceptical about moving into a risk and compliance role. However, I quickly learnt the importance of the role and the value it can add across an organisation. My time as a Regulator was an apprenticeship into all aspects of issues within financial services and gave me a broad insight to the challenges of all businesses, large and small. When I left, I wanted to share back what I had learnt to help strengthen the industry and provide a plain English perspective on governance, risk and compliance.

What area of compliance do you think Financial Advice Providers (FAPs) need the most help with? Do you see any changes to this with the new government coming in?

From our experience, most FAPs and their advisers still don’t really know the extent of their new regulatory obligations. I expect that the FMA will start to publish guidance to assist FAPs with implementation and help them mature their approach to complying with the regime. The Conduct Licensing is a great addition for New Zealand as it helps us lift our game for product providers and is great for consumers. Hopefully, the government has other priorities and lets the industry get on with meeting the fair conduct principles.

Could you tell us a bit about what your compliance and governance courses cover?

Over the last few years, we have been running course and coaching new Compliance Officers. Often the person has been thrown in the deep end and needs to have both the theoretical and practical understanding of their role. This year we added a focus on oversight and ran practical governance and compliance courses. The blend of running both together means that the business owners/directors can work through responsibilities with their compliance person and come with clear workplan for 2024.

What is one thing you wish someone had told you when you were younger?

To follow your passion and back yourself. I always knew that I wanted to run my own business and now wish I had got underway sooner. In saying that, I have loved every company I have worked for and each has taught me so much. It’s always the people around you who make the difference.

What’s the last book you read?

I just finished “Resurrection Walk” by Michael Connelly. It is part of a series about the characters of the Lincoln Lawyer Mickey Haller and Detective Harry Bosch. These books are now series on Netflix and so I had a resurgence of interest in reading the latest books! Easy holiday reading!

Disclosure: Quality Product Research Limited has used the services of Rosewill Consulting Limited and found them to be excellent.

More daily news:

Westpac wins five awards at the KangaNews Awards 2023

George Crosby has been appointed as the new chief investment officer for ANZ Investments

Australia’s Federal Government seeks feedback on the use of genetic test results by insurers

Australia’s Federal Government has opened consultation on the impacts of life insurers utilising genetic test results in underwriting.

Under the Insurance Contracts Act 1984 consumers have a responsibility to provide information requested by life insurers, including any genetic testing results. In 2018, a report by the Parliamentary Joint Committee on Corporations and Financial Services identified concerns that life insurers using genetic tests in underwriting was negatively impacting participation in health research projects involving genetic testing.

In 2019, Australia’s life insurance industry introduced a partial Moratorium on the requirement to disclose genetic testing results. Life insurers could only request or use the results of a genetic test if the total amount of cover a person has exceeded set thresholds. The Moratorium also stated that life insurers would not require or encourage applicants to take a genetic test as part of the application. The Moratorium was introduced due to concerns that people would not undergo genetic testing for personal health reasons or participate in medical research that involved genetic testing because they feared that it could negatively impact their ability to obtain affordable life insurance.

A report by researchers at Monash University investigating the impact of the Moratorium found it is discouraging consumers from participating in clinical genetic testing and in medical research which involves genetic testing. The report also found that life insurers were not complying with the Moratorium, and were asking applicants about genetic test results when the applications fell below the financial thresholds. The report also deemed the financial limits were too low. The report’s recommendations include the Government amending legislation to prohibit insurers from using genetic or genomic test results to discriminate between applicants for risk-rated insurance and that the Government consider ensuring insurers are subject to a positive duty to not discriminate. Consultation is open until 31 January 2024.

We spoke to Russell Hutchinson to get a New Zealand perspective on this issue:

Currently New Zealand has no legislated approach to genetic testing. There are similar consumer movements to that in Australia, which highlight the risks to consumers and their families when they delay obtaining genetic tests because they are concerned about the impact on their ability to obtain insurance coverage. A good synopsis of this from the medical viewpoint is given in this Radio New Zealand piece. It does not discuss the value of having a functioning insurance sector or examine how this relies on the ability to charge different premiums for different risks or in some cases, decline to insure a person. Naomi Ballantyne offers a succinct summary of an underwriter’s perspective in this article at Good Returns.

Occasionally, consumer fears may drive choices which are also damaging to the insurance market – for example, delaying a test to take out coverage and then lapsing the coverage if the test results show no increased likelihood of developing the condition. There may be value in offering some form of reassurance to consumers to limit the impact of genetic testing on insurance. Personally, right now, I would encourage anyone contemplating a genetic test to place their health first and obtain the test.

The Financial Services Council (FSC) regularly reviews its stance and industry guidelines on genetic testing to ensure they reflect best practice globally; they have reiterated that it is important insurers understand a customer's risk profile as part of the underwriting process.

"Some insurers may ask customers to disclose known information about the results of their genetic tests. This is consistent with asking customers other questions about their risk profile - for example, their family history.”

"Genetic testing is not something that any of our members ask their customers to carry out. Overall, FSC believes a fair position is one that balances the interests of consumers and the medical community to advance genetic science, and which manages financial risks to insurers and all policyholders."

Recently the FSC has held a discussion group with representatives from the insurance industry and the medical community to discuss the challenges that genetic testing present. A working group has been established to improve outcomes from genetic testing. Currently, RiskInfoNZ is running a poll to find out if people will see a time when genetic tests will play a part in clients applying for life insurance.

More daily news:

Gold Band Finance is the first non-bank deposit taker to get an FMA Financial Institution Licence

Proposed changes to the NZCFS Level 5 will be published on the Ringa Hora website early next year

Legal and regulatory update for the life and health insurance sector

27 Nov 2023 - APRA embarked on a multi-year pilot study with a selection of banks to gain insights into the status of data risk management. They have outlined their findings and highlight multiple areas where all APRA-regulated entities can improve their data management practices. https://www.apra.gov.au/news-and-publications/quality-data-as-an-asset-for-boards-management-and-business

28 Nov 2023 - The Financial Markets Authority (FMA) has cancelled Foundation Advice Limited (FAL)’s Financial Advice Provider (FAP) licence. FAL was an Auckland-based FAP offering advice on life and health insurance as well as KiwiSaver. The High Court put FAL into liquidation on 26 October 2023 following an application filed by the Inland Revenue Department. https://www.fma.govt.nz/news/all-releases/media-releases/fma-cancels-foundation-advice-limiteds-licence/

28 Nov 2023 - ASIC has issued guidance to financial advisers and Australian financial services (AFS) licensees about the new requirement for financial advisers to be registered. From 1 February 2024, financial advisers who provide personal advice to retail clients on relevant financial products must be registered with ASIC. https://asic.gov.au/about-asic/news-centre/news-items/asic-releases-guidance-on-the-registration-of-financial-advisers/

28 Nov 2023 - The FMA has agreed in principle to grant a class exemption for five years for each Climate Reporting Entity (CRE) which is in liquidation, receivership or voluntary administration from the duties in Part 7A of the FMC Act, comprising:

full relief for a CRE which is in liquidation (solvent or insolvent) and for managers that are CREs in respect of a registered scheme (or fund within a scheme) that is in wind-up.

deferral relief for up to two years for CREs in receivership or voluntary administration.

The effect of full relief is that the climate reporting duties are cancelled. The effect of deferral relief is that climate reporting duties are deferred but must still be complied with at a later date.

Changing business demographics opens up opportunities for advisers

Stats NZ’s latest business demography statistics (as at February 2023) paints a promising picture of New Zealand’s economic landscape. With more new businesses and a rise in employment, opportunities abound for insurance advisers specialising in Business Risk Protection products.

Stats NZ’s latest business demography statistics (as at February 2023) paints a promising picture of New Zealand’s economic landscape. With more new businesses and a rise in employment, opportunities abound for insurance advisers specialising in Business Risk Protection products.

Key highlights include:

· The number of enterprises in NZ is following an upward trajectory, with 605,000 enterprises in February 2023, up 1.8% from February 2022. This is on top of a 5.3% increase in the year to February 2022.

· The number of paid employees in these enterprises (not an official employment statistic) was 2.5 million, up 3% from February 2022.

· These enterprises operated across 641,560 business locations, up 1.4% from February 2022.

There has been a marked increase in new businesses across a range of sectors, indicating a healthy and growing economy. The data also reveals a positive trend in employment, with employees in large enterprises up 5.9% from February 2022.

Ministry of Business Innovation and Employment figures show 196,584 people entered NZ on work visas in the 12 months to September, up dramatically from 39,501 in the 12 months to September 2022. The arrival of these overseas workers further increases the pool of workers available and makes it much easier for employers to fill any vacancies.

Certain industries, such as construction; professional, scientific and technical services; and health care and social assistance industries, have shown significant growth. These sectors often have specialised insurance requirements, like protecting shareholder needs or covering key people within an organisation, providing a niche market for advisers.

Quality Product Research Ltd have recently completed independent research on Business Insurance lump-sum products, putting a wealth of information at advisers’ fingertips in order to make well-informed recommendations. With disability products soon to be included, advisers can offer a comprehensive suite of options to their clients.

Advicemonster has functionality that allows users to streamline the process of creating Business Statements of Advice (SOAs), speeding up the time spent on admin and freeing up more time to spend with clients. Please get in touch if you’d like a sample copy of a Business SOA. Advicemonster’s tools assist advisers in conducting a Fact Find and Needs Analysis and being able to offer highly personalised solutions.

The combination of up-to-date research and specialised tools allows advisers to educate new businesses on effective risk mitigation strategies. This is particularly crucial for sole traders and SMEs that may not yet be aware of the full range of risks they face.

To find out more about what Advicemonster can do for you, please contact Aneel Ravji on 0212160905 or ask us about our next online training sessions.

Swiss Re write about redefining sustainability in life and health insurance

Daisy Ning, Head Life & Health Re APAC ex. China, writes about how sustainability can be applied more broadly in the insurance and reinsurance context. Swiss Re believe sustainability aligns with what they refer to as the ‘3A’s’ of life and health insurance:

accessibility (the ease of acquiring coverage), availability (whether suitable plans and products exist to cover the full range of L&H needs), and affordability (whether products and plans are priced fairly and within consumers’ means).

Ning advocates for formulating strategies that manage risk, improve adaptability and explore opportunities – regardless of market conditions; assessing trends and value delivered to clients and adjusting as necessary; and enhancing value delivered to clients by making insurance solutions more relevant.

The global protection gap in 2022 was sitting at US 406 billion in premium equivalent terms, up 1.5% since 2021. A recent Deloitte estimate has the Australian public at 60 – 80% underinsured. A Swiss Re estimate of NZ’s mortality protection gap was USD 435 billion (NZD 670 billion) or more than USD 540 000 for each household, as of 2020.

Ning suggests we need to leverage connectivity and digitalisation to make products more affordable; leverage big data and advanced analytics to uncover insights into market trends, customer behaviour and risk factors and create products that address emerging needs discovered through this process; look at digital health underwriting; and increase reach through building alliances with online platforms, aggregators, fintechs and other digital players.

More daily news:

Katrina Shanks works through pros and cons of Trusts

Industry leaders suggest how incoming government can support the industry

mySolutions launches New Adviser Academy

FintechNZ Annual Meeting 2023 3pm on 23 November

ANZ awarded New Zealand's top bank for small business by Canstar NZ

Link financial group awarded one of the Best Mortgage Companies to Work for in New Zealand

nib release 2023 sustainability, community and climate-related disclosure reports

nib Group have released their 2023 sustainability, community and climate-related disclosure reports. Some highlights from the reports include:

· 25,990 HealthChecks were undertaken by nib members.

· Employee Experience Surveys in FY23 found an overall engagement score of 81%.

· 289 staff volunteered 1,546 hours across 14 charities.

· 34 suppliers completed continuous improvement plans to manage modern slavery risk.

· The strategic procurement team has taken a proactive step toward reducing nib’s carbon footprint by introducing environmental criteria into the Request for Proposal (RFP) process.

· nib introduced a new values-based employee recognition program where all employees have the opportunity to nominate their colleagues and vote on the most extraordinary achievements.

· nib worked with Ngāti Whātua Ōrākei to facilitate the ‘Cultural Coalition’ Program (Whatua te Aho Tukurua). This six-week program teaches participants Māori language and values, encouraging employees to integrate these learnings into regular work activities and practices.

· Gender pay equity gap has reduced to 2.75%.

· 985 Kiwis visited Clearhead’s Te Reo Māori website and chatbot

nib has identified climate-related risks including:

· increased market pressure to provide community support and insurance affordability for those experiencing climate hazards;

· increased illness & comorbidity due to chronic and compounding climate change hazard;

· trauma, illness, property destruction and disruption leading to high rates of psychological distress;

· increased incidents and severity of climate hazards causing pressure on discretionary income;

· chronic and compounding climate change impacts putting pressure on health services;

· energy and emissions performance standards creating compounding capital expenditure and operational costs;

· limitations of current regulatory and pricing mechanisms to respond to climate hazards;

· risk nib won’t meet growing mandatory reporting and regulatory requirements.

nib has developed a risk-management framework to manage and mitigate its material risks, and their board and management regularly identify and analyse risks and the effectiveness of the controls in place to manage these risks.

More daily news:

FinTech NZ is asking members to fill in their 2024 New Zealand Fintech Pulsecheck Survey

mySolutions webinar 'Roles and responsibilities of Directors' 9am 18 October

Open letter to Pharmac saying the chief executive and the chairman need to step down

Q&A with the Financial Advice NZ Risk Board Member Director (Risk) nominees

Sonja is self-employed, working under the SHARE FAP, advising clients on Risk and KiwiSaver investment. Sonja has over 20 years’ experience in the Financial Services industry and is also a Director at Habitat for Humanity, a Chairperson for Migrant Connections Taranaki Charitable Trust and a Justice of the Peace.

What attracted you to the insurance industry?

I love the flexibility and lifestyle that the industry offers, especially when you are self-employed, as well as the social aspect, meeting new people/clients, some of whom become lifelong friends.

If you were elected Member Director (Risk), what would your key priorities be?

Key priorities for me would be looking at a pathway for young people to join the industry, continuing to educate and assisting advisers navigating the new regulatory environment as well as looking at new strategies to maintain and enhance the wellbeing of advisers.

What is one thing you wish someone had told you when you were younger?

The one thing I wished someone had told me: don't sweat the small stuff… we worry about too many things sometimes, instead of looking at the big picture.

What’s the last book you read?

I read a lot of books, but the last book I read is 'Sand talk" by Tyson Yunkaporta, the author asks what happens if we bring an indigenous perspective to the big picture - to history, education, money, power? Can we, in fact, have proper concepts of sustainable life without Indigenous knowledge? He challenges us to think differently - a great read I picked up on my last visit to Sydney.

Zebunisso Alimova

Zebunisso has a variety of experience in the financial services sector, starting off in banking and now owning a Mike Pero Franchise. Zebunisso was recognised as one of MPA’s top advisers in New Zealand 2022 and 2023.

What attracted you to the insurance industry?

The insurance industry, in my view, represents a unique intersection of financial services, risk management, and the profound impact it can have on individuals and businesses. What truly attracted me to this industry is the opportunity it provides to make a real difference in people's lives. Insurance is about offering peace of mind, security, and a safety net when the unexpected occurs.

My journey into insurance began during my tenure at ASB Bank, where I witnessed firsthand how crucial insurance products were to our clients' financial well-being. I was drawn to the industry's ability to provide tangible protection against life's uncertainties, whether it's safeguarding a family's future, ensuring the survival of a business during challenging times, or offering stability in retirement.

Moreover, insurance isn't just about selling policies; it's about building trust, understanding clients' unique needs, and tailoring solutions to fit those needs perfectly. This client-centric approach resonated deeply with me, aligning with my core values of empathy and service.

The insurance industry is dynamic, constantly evolving to meet the changing needs of our society. This dynamic nature challenges me to continually learn, adapt, and innovate, making each day in the industry an exciting and fulfilling experience.

If you were elected Member Director (Risk), what would your key priorities be?

If I have the privilege of being elected as Member Director (Risk), my key priorities would revolve around enhancing the overall risk management framework within Financial Advice New Zealand. I believe that a proactive and comprehensive approach to risk management is essential for the sustainable growth and success of any organization. Here are some key priorities I would focus on:

1. Fresh Perspectives and Strategic Thinking: As mentioned in my video statement, I aim to bring fresh perspectives and strategic thinking to the role of Member Director (Risk). This approach involves looking at risk management from new angles, exploring innovative solutions, and ensuring that our risk management strategies align with our strategic objectives.

2. Diplomatic Voice for Collaboration: In the video, I emphasized the importance of maintaining a diplomatic voice that fosters collaboration and consensus-building within the organization. Effective risk management often requires input and cooperation from various stakeholders. I would work diligently to ensure that all voices are heard and that decisions are made with the best interests of the organization in mind.

3. Addressing Industry Challenges: I am acutely aware of the challenges the industry is currently facing, such as the struggle to attract young talent due to evolving regulations. These challenges were discussed in my video statement, and I am committed to addressing them both as a business owner and as an advocate for our industry's growth. This includes exploring ways to make our industry more appealing to emerging professionals.

4. Client-Centric Approach: Just as I emphasized the importance of a client-centric approach in my video statement, I believe that risk management should ultimately serve the best interests of our clients. This means ensuring that our risk management practices protect our clients while also allowing them to access the products and services they need.

What is one thing you wish someone had told you when you were younger?

If I could impart one piece of wisdom to my younger self, it would undoubtedly be the importance of securing a fixed-rate loan when interest rates were historically low, such as the opportunity to fix the loan for five years when rates were at 2%. This financial decision can have a significant impact on one's long-term financial stability and mortgage affordability.

Understanding the intricacies of interest rates and financial planning early in life can empower individuals to make informed decisions that set them on a path to financial security. It's a reminder that even seemingly small financial choices can have a substantial cumulative effect on one's financial well-being over time. Planning for the future, whether through smart borrowing or prudent saving and investing, is a key lesson I've learned and would encourage others to embrace.

What’s the last book you read?

The last book I read was "French Village Book Lovers." This delightful book by Martin Walker takes readers on a journey through the charming villages of rural France. It's a captivating exploration of the intersection between French culture, history, and the love of literature. As someone who values cultural diversity and the enrichment that comes from literature, this book was a delightful and enlightening read. It reinforces the idea that books have the power to connect us with different worlds and broaden our perspectives, much like the diverse and dynamic field of finance, which I'm passionate about.

More daily news:

Good returns article lists some pros and cons to AI use in the financial services industry

The primary test for cervical screening has changed to a HPV test, with the option of self-testing

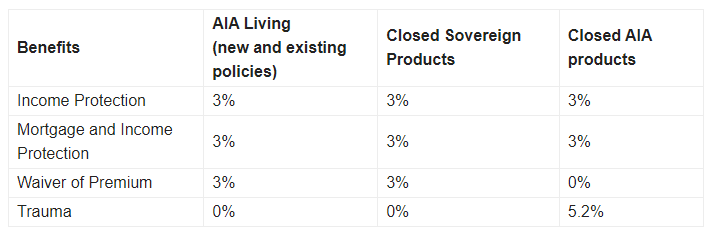

Premium increases at AIA

AIA is increasing premiums on its income protection (IP), waiver of premium and closed trauma products. AIA have said the increases are based on a gradual increase in IP claims and a higher level of claims on closed AIA trauma products compared with their wider trauma portfolio.

The table below shows the pricing increases, with closed AIA trauma products set to have staggered price increases at a rate of 5.2% a year over the next three years.

More daily news:

Tony Vidler recommends advisers keep client consultations simple

The IMF says the NZ Government needs to trim spending or risk prolonging high inflation

Banking ombudsman recommends changes to loan application processes

MyLifeMatters campaign calls for new medicines and more Pharmac investment

Legal and regulatory update for the life and health insurance sector

28 Aug 2023 - The Reserve Bank has introduced a new data series called New Residential Mortgage Lending by Purpose https://www.interest.co.nz/personal-finance/123983/number-people-choosing-top-their-home-mortgage-running-fewer-half-number

28 Aug 2023 - ASIC’s latest Corporate Plan reveals ASIC will take further enforcement action to protect Australian consumers and small businesses in an environment where scams, digitally-enabled misconduct and predatory lending practices are increasingly prevalent https://asic.gov.au/about-asic/news-centre/find-a-media-release/2023-releases/23-230mr-asic-focuses-on-protecting-vulnerable-consumers-and-small-businesses-in-23-24/

29 Aug 2023 - APRA has unveiled its 2023-24 Corporate Plan, which outlines an evolution in APRA’s priorities for the coming four years in response to new and developing risks impacting the global financial system https://www.apra.gov.au/news-and-publications/apra-responds-to-emerging-risks-2023-24-corporate-plan