Chatswood serves the life and health insurance sector in New Zealand with market intelligence, data, and bespoke consulting services. Some of these are provided in conjunction with Quality Product Research Limited - a subsidiary that brings you Quotemonster.

We believe that good decisions are more likely to occur when we have good information about the market environment in which we operate. Intuitive leaps and creative decisions are always required, of course, but the more they are based on a firm foundation of observation, the better they tend to be.

Research updates: what you need to know!

QPR Database V15.2A released

Our Research team have made some monstrously good updates to the QPR database recently. If you’ve noticed we’re running a bit slower than usual, please refresh your page and scroll down to ensure that you’re on our latest version – QPR V.15.2A | WEB V4.3.9.

Our latest updates include:

Cigna rebrand to Chubb Life – this has been live on Quotemonster since the brands launch in March, however all rebranded documents can now be accessed by database subscribers.

Kiwibank rebrand to nib effective 1 June 2023 – more information on this here.

MAS - policy document update for Life & Income Protection effective 1 December 2021, with product rating changes in Income Protection (indemnity) – rating applied in Vocational and Rehabilitation Support .

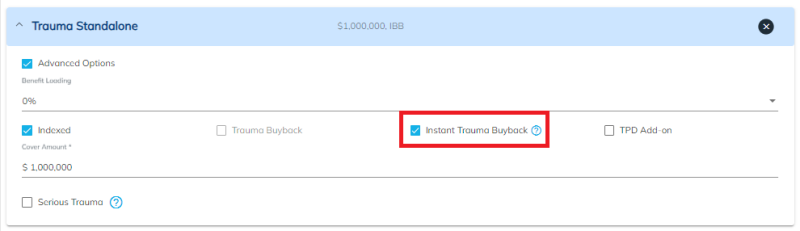

Research for Partners Life Immediate Trauma Buyback and Asteron Life’s Continuous Trauma is available when Instant Trauma Buyback is selected.

ANZ – policy document update for Life & Living effective 6 March 2023, however, this has not affected product ratings.

Other Research remediations include:

Medical: Exclusions

Income Protection: Insurable Income and Inflation Adjustment

Trauma: Heart Attack

TPD: Benefit Definition over 65

If you have any questions regarding these please feel free to email us on info@quotemonster.co.nz

Happy Crunching!

Updated premium comparison tool includes new Fidelity Life rates, offer, and new nib life and living package

We have updated and sent out a new Life Premium Comparison database to all our institutional subscribers.The new version is v120.

Changes in this version :

Updated Fidelity Life IP, MP and Trauma (YRT and Level) rates effective 1/6/23

Removed Fidelity Life policy fee (temporarily waived until 31/8/23)

Added nib Life & Living rates effective 1/6/23 (YRT Life, Trauma Standalone and Income Protection)

There are some other announced, but not yet implemented, rate changes coming. Keep an eye out for the updates as those get released to the market.

Quick - join us! Advicemonster Demo with Aneel!

Over 1,600 Statement Of Advice (SOA) reports have been generated on Quotemonster in the last six months and we invite you to see why!

We welcome you to join our upcoming online Advicemonster training session scheduled on Friday, 16 June 2023 2:00 pm-3:00 pm.

In this session, we have an in-depth walk-through of our Statement of Advice service and how you can create a professional and comprehensive SOA. Be the first to learn about our recent enhancements and ongoing developments from our new AdviceTech Lead, Aneel Ravji. Our Needs analysis and SOA tools are exclusive to the Advicemonster subscription and due to the advanced nature of the product, training can take between 60-90 minutes. This session is great to attend for those considering upgrading their subscription, or if you have already upgraded but would like to learn how to get the most out of it.

If you would like to register, please send us an email on info@quotemonster.co.nz

We look forward to seeing you there!

Quality Product Research: Major Review of Trauma Incidence

According to the FSC, in 2020, a total of $113,700,000 trauma claims were paid out in New Zealand, accounting for 20% of risk claims paid out at the time. Quality Product Research (QPR) uses reinsurer claims information to weight our scoring according to the most important items. For example, 80-90% of our trauma weighting is given to high claiming conditions and the remaining is evenly distributed between minor conditions.

Our incidence factor aims to reflect how likely a benefit will be claimed and is vital within trauma, currently females have an incidence of 69.17% for cancer, while this number is 43.46% in males. Failing to consider this factor would affect the value of certain benefits - we aim to have the incidence rate in our model closely track actual claims to provide a real value-based approach to rating.

Our four-factor research considers four features in our overall score:

Definition x Incidence x Amount x Frequency = Insurance Quality Score

For more information on our methodology please click here.

Based on the most recent claims data from Gen Re, we have reviewed our Trauma Incidence Scores and openly welcome your feedback on these. Please find attached:

A comparison of current and proposed trauma incidence – click here to view (excel file).

A trauma incidence infographic – click here to view (pdf).

Your feedback

We value getting your feedback on how these wordings are being applied to claims you may be aware of. Please email us with details of any recent claims to assist with our ratings.

Doreen Dutt, Quality Product Research Limited, researcher@qpresearch.co.nz

Legal and regulatory update for the life and health insurance sector

9 Jun 2023 - ASIC has granted relief to life and general insurers to provide modifications and exemptions from the confirmation of transaction requirements contained in section 1017F of the Corporations Act in prescribed circumstances. The relief will expire on 1 July 2028.

Confirming transactions – deceased life insurance policyholder

This relief seeks to address situations where it may not be appropriate and/or necessary to confirm transactions with the holder of a life insurance policy where the life insurance policyholder is deceased and there is no alternative holder of the product.

Confirming transactions – recurring insurance benefit payments

For certain recurring benefit claims, this relief seeks to facilitate life and general insurers providing confirmation in the form of a statement given before, rather than after, the transactions are made. This includes benefit payments where the holder of the product is unable to work because of illness, injury or unemployment.

13 Jun 2023 - ASIC invites Australian entities to take part in the ASIC cyber pulse survey to measure cyber resilience https://asic.gov.au/about-asic/news-centre/find-a-media-release/2023-releases/23-160mr-asic-invites-australian-entities-to-assess-their-cyber-resilience/

13 Jun 2023 - NZ Police Financial Intelligence Unit released “The Suspicious Activity Report” for April 2023 https://www.police.govt.nz/sites/default/files/publications/fiu-monthly-report-apr2023.pdf

13 Jun 2023 - The Reserve Bank of New Zealand has released its finalised risk weighting decisions and response to the points raised in submissions. They have also published an Exposure Draft of the associated Banking Prudential Requirements (BPR) document that covers the technical changes needed to implement the decisions. https://www.rbnz.govt.nz/hub/news/2023/06/further-decisions-on-bank-risk-weights-released

14 Jun 2023 - Minister of Finance, Hon Grant Robertson, May 2023 diary released with the following potential financial services sector related meeting noted:

• 1 May 2023 – Ministerial meeting with RBNZ officials, Treasury officials

• 12 May 2023 – Speech at BNZ pre-Budget event

• 12 May 2023 – Speech at Centre for Sustainable Finance CEO roundtable

• 19 May 2023 - Speech at ANZ post-Budget event

• 22 May 2023 – Meeting with RBNZ

• 24 May 2023 - Call with RBNZ

https://www.beehive.govt.nz/sites/default/files/2023-06/Ministerial%20Diary%20May%202023.pdf

Quality Product Research: FAQ – can research ratings be altered?

We hope this explanation can provide more clarity on how our research works.

Our objective is to be a tool for advisers to highlight the material differences between products, rather than a view of ranking them from best to worse, therefore, advisers are able to select their product and provider basket to what they are qualified to advise on (i.e., they can remove providers and alter products where required). However, in reality, price is also a significant factor during the advice process and both our pricing comparison and research rating are used by advisers to justify why a selection is being made - along with other information and views you may have, of course.

For example, ideally an adviser will select all agreed value base products under non-taxable (agreed value).

In this set, Partners Life may have a research rating advantage, but pricing disadvantage, assuming current settings.

If an adviser then decides they want to remove Partners, for whatever reason (perhaps they have no accreditation with them), this removes Partners Life from being shown in the premium comparison however, it would be inaccurate to then bump AIA to 100% because in this specific set Partners Life still has the highest score.

When it comes to Options and Extras packages, in an ideal world, an adviser would select the best products in the set to compare and again will have to consider the pricing comparison and research rating as a package.

Fidelity has a pricing advantage (cheapest in this set) and a research advantage in this example below.

However, removing Fidelity will remove the provider from appearing in the premium comparison, but it will not alter the research comparison – they still have the highest rating in the set and the other companies are benchmarked against this.

We believe it would be inaccurate if advisers were allowed to remove a company to then alter research ratings. They can, however, alter products but have to be able to justify it from a pricing and rating perspective.

We hope this provides some insight into how research ratings work and if there is a specific topic you would like us to share on, please send us an email on info@quotemonster.co.nz

Questions answered: does everyone already have a life insurance policy?

Question from a reader:

The FSC have released their quarterly life insurance snapshot FSC SPOTLIGHT Life Insurance MAR 2023.pdf (hubspotusercontent-na1.net). What I found particularly interesting was there are 4.1 million life insurance covers and New Zealand has about 5.18 million residents. Stats NZ has 986600 people under 15 in 2021 national-population-estimates-at-30-june-2021.xlsx (live.com), and I would assume most under 15 year olds wouldn’t have (or need) life insurance. So, are we basically at market saturation now? Or are there a large number of people with multiple life insurance policies?

Answer:

At Chatswood we do not think that everyone has a life policy and you are right to suspect that multiple policies is a likely explanation. For example, at one point I had five policies with Sovereign, that was a consequence of how increases and additions were done. At the same time I had some group life insurance in the staff scheme, so that made it six. I may have had some credit card insurance too. We work on an average of between two and three policies per person, which leaves the uninsured at about 50% of the working age population. The FSC has also recently done a survey of consumers and their answers indicated that the coverage rate is about 38%. However, consumer surveys about low engagement products such as life insurance are particularly susceptible to response biases. I explore some of these issues in my recent article at goodreturns 'why is is so hard to know how many people have life insurance?' If you would like a more detailed approach to this with the associated modelling and sources please contact us for a copy of our special report on market size and flow.

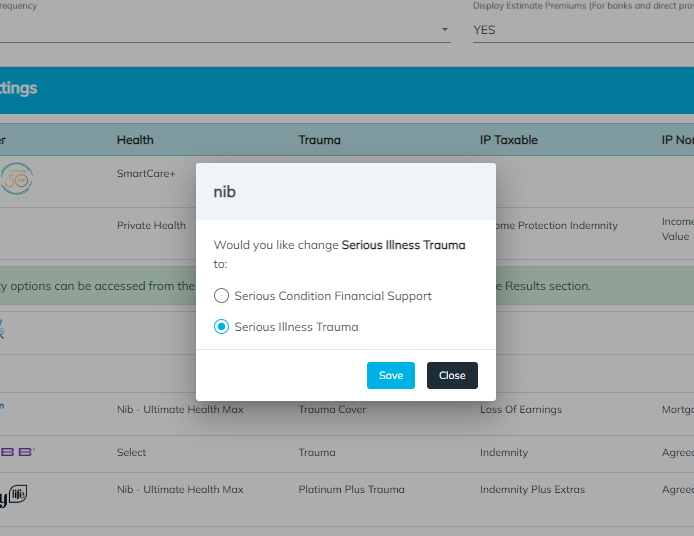

The addition of nib Life & Living to Quotemonster!

We have recently updated Quotemonster to include nibs Life & Living products.

In the Product and Provider Settings, you’ll find the usual options for nib under Health, and now you’ll be able to include Life & Living Life, Trauma and Income Protection in your pricing and research comparisons. This also means that you’ll be able to quote a package for this provider.

Note that we have included both the Serious condition Financial Support option (only available for sum insureds of $20,000 or $50,000) and Serious Illness Cover to select from in Trauma.

Click here to read more on this topic in Insurance Business, which also includes an interview with Chris Carnall, nibs Adviser Distribution Head, and you can click here to register for nibs national roadshow.

If you have any questions or feedback on this topic, please feel free to contact us on info@quotemonster.co.nz

Quality Product Research: Research Ratings Terminology

If you’ve ever seen the terms Total Benefits Score or Total Weighted IQ Rating on Quotemonster and wondered what they meant, you’re not the only one!

Here is some information on numbers and terminology which we hope will provide you with a better understanding of our Research.

For a product (e.g., Life Cover), the Total Benefits Score (Image 1) is the sum total of every benefit being rated. You can view the entire list of benefits by ordering your Research Alphabetically.

Image 1:

The Percentage Rating (Image 1) converts to a Star rating for each insurer’s products and is also provided in this screen.

In the example above (Image 1), the highest total benefits score is 106.44, which belongs to AIA, therefore this company has a Percentage Rating of 100% and is a 5-star product. Next, the other products are benchmarked against this as below:

Chubb Life: 104.76/106.44 = 98.4% rounds to 98%

Fidelity: 104.50/106.44 = 98.2% rounds to 98%

Partners Life: 106.02/106.44 = 99.8%, rounds to 100%

The Percentage Rating is then converted into a Star Rating according to our table below:

When ordering by Importance, we aim to only present the high scoring benefits for the selected product, and all others are combined and displayed in the Secondary Benefits Score (Image 2).

Again, to see every benefit, simply order Alphabetically.

Image 2:

Researchmonster subscribers have the additional Research tab, which defaults to the Package Score and includes the term Total Weighted IQ Rating.

IQ = Insurance Quality and we highly recommend referring to our Why Methodology Matters infographic for detailed information and you can click here to download this.

To get the Total Weighted IQ Rating, the Total Benefits Score for each product is multiplied by the Product Line Weighting Factor*

*In reality, the distribution of claims differs based on age, gender, and other factors. Our Product Line Weighting Factor aims to model the relative weight of a claim and as we know, models aren’t an exact science.

In our example below (Image 3), Chubb Life: 104.76 (Total Benefits Score) x 0.1 (Product Line Weighting Factor) = 10.48 (package score for Life cover).

This is completed for each benefit and totalled to form the Total Weighted IQ Rating (Image 3).

Life 10.48 + Trauma 31.85 + Health 10.42 + Mortgage 14.37 + TPD 14.97 + Income 19.21 = 101.30

Star ratings (aka Percentage Rating) for the package is also provided in this screen.

In this set, the highest score is 102.85, which belongs to Partners Life, therefore this company has a Percentage Rating of 100% and offers a 5-star package suite. Next, the other products are benchmarked against this as below:

AIA: 101.66/102.85 = 99%, Chubb Life: 101.30/102.85 = 98%, Fidelity: 100.01/102.85 = 97%

Image 3:

We hope this provides some insight into how research works and if there is a specific topic you would like us to share on, please send us an email on info@quotemonster.co.nz

Fidelity Life’s premium changes are now live!

We are pleased to confirm that the premium changes to Life, Trauma and Income Replacement covers for Fidelity Life, effective 1 June 2023, are now live on Quotemonster.

Fidelity is waiving policy fees effective 1 June to 31 August 2023 and Quotemonster also reflects this offer.

To read more on this, please click here.

Happy Crunching!