Chatswood serves the life and health insurance sector in New Zealand with market intelligence, data, and bespoke consulting services. Some of these are provided in conjunction with Quality Product Research Limited - a subsidiary that brings you Quotemonster.

We believe that good decisions are more likely to occur when we have good information about the market environment in which we operate. Intuitive leaps and creative decisions are always required, of course, but the more they are based on a firm foundation of observation, the better they tend to be.

Fidelity Life announce premium changes

Effective from 1 April 2025, Fidelity Life are re-rating the premiums for customers in the Adviser channel.

Effective from 1 April 2025, Fidelity Life are re-rating the premiums for customers in the Adviser channel. Key aspects are below:

A re-shaping of the pricing curve to reflect a lower risk due to the underwriting selection effect.

A 5% increase to all lump sum premiums and disability premiums (where the benefit period is 2 or 5 years). And a 7.5% increase to all disability covers with a benefit period of ‘to age 65’ or ‘to age 70’ due to claims experience.

An adjustment of the rates for all customers.

More news:

Jon-Paul Hale suggests reasons for medical premium increases

Fitch has lifted the outlook on ASB's credit rating to positive from stable

ANZ-Roy Morgan’s report shows consumer confidence has dipped to 93.2

The Reserve Bank is considering loosening its bank capital rules

AI becoming more trusted by executives

SAP investigated how US executives were using AI in their organisations and their trust in the technology.

SAP investigated how US executives were using AI in their organisations and their trust in the technology. They found that AI has become embedded in work practices (with 63% of executives using generative AI daily) and is changing how people do business.

Decisions are being made based on AI insights, with 44% of C-suite executives saying they would override a decision they had already planned to make based on AI insights and another 38% trusting AI to make business decisions on their behalf. 74% of executives had more confidence in AI advice over advice from family and friends. And a massive 55% of executives say in their company AI-driven insights have replaced or bypassed traditional decision-making.

Some common tasks carried out by generative AI tools include:

Analysing data and making recommendations for decision-making (52%)

Spotting risk or issues they hadn't previously considered (48%)

Offering alternate plans (47%)

Enhancing product development (40%)

Supporting budget planning (40%)

Performing market research (40%)

SAP found that there were positive implications on employee wellbeing, with 39% of executives reporting better work-life balance, 38% reporting improved wellbeing and 31% reporting reduced stress.

More news:

SortMe Advisor Portal, a tool designed to enhance financial advisory services, launches

AIA launch new Guide to Medical Underwriting

28% of large organisations rank AI-generated cyber threats as a major risk

Munich Re delve into AI’s impact on Healthcare

Munich Re delve into the projected impact of Artificial Intelligence (AI) on healthcare, from disease prevention to diagnosis to treatment as well as the implications for efficiency gains.

As part of Munich Re’s Life Science Report, they have investigated the projected impact of Artificial Intelligence (AI) on healthcare, from disease prevention to diagnosis to treatment as well as the implications for efficiency gains.

While the news is mostly good (improved mortality, better prevention, earlier diagnoses, individualised therapies), it does create some challenges for life and health insurers. With earlier diagnoses and the emergence of new disease classifications, critical illness insurance products will need continuous updating. Claims management and policy development will become more complex, as genetic and molecular diagnosis becomes more routine, requiring a higher level of medical expertise. Overdiagnosis (the detection of diseases that don’t impact on mortality and/or morbidity) and antiselection may become problematic.

AI will also create opportunities for insurers. Insights from accessing and analysing vast datasets including electronic health records, imaging and other biomedical sources will transform the understanding of the root causes of disease and in turn allow underwriting to become more accurate and sophisticated. Wellness interventions will be able to be better targeted and increase in scope and effectiveness.

More news:

Profile of Josh Bronkhorst, CEO of Link Financial Group

Entries for Insurance Business’ annual Top Insurance Employers close 14 March

InvestNow’s Retirement Readiness Index recorded an average confidence level of 50.4%

Kiwibank reports NPAT of $92 million for the six months ending 31 December 2024

New framework moves beyond traditional reliance on BMI as a sole indicator of obesity

Chubb Life introduce Smart Start, Change of Mind and the ability to delete quotes

Chubb Life have announced the launch of their new “Smart Start” feature, a new “Change of Mind” window for cancellations and withdrawals and the ability to delete quotes in Adviser Hub.

The Smart Start feature will be rolled out from 13 – 20 February. With “Smart Start”, once underwriting for an Assurance Extra or Assurance Extra Business policy has been completed at standard rates or an Offer of Terms has been accepted, Chubb Life’s systems will initiate a temporary pause period and advisers will receive a “Ready to Issue” email which outlines the planned commencement date, first payment date, payment frequency and premium amount. The default pause period is five working days, after which the policy will automatically issue, though advisers can adjust the pause period to anything from 0 – 5 days. During the pause period, advisers can request changes by replying to the email or calling the New Business team.

From 14 February, cancellation requests will be processed as soon as they’re received and the “Change of Mind” 14-day window will apply, whereby customers will be able to withdraw their cancellation request and retain their cover without going through underwriting again. If customers were to experience a claimable event, they’ll continue to be protected until the end of the change of mind window, or the effective date of the cancellation, whichever is the latest.

Advisers will be able to delete quotes from AdviserHub – individual quotes can be deleted from within the quote itself, or advisers can delete multiple quotes through a bulk delete function on the “retrieve quote” screen.

In other Chubb Life news, AM Best has reaffirmed Chubb Life Insurance New Zealand Limited's Financial Strength Rating of A (Excellent) and Long-Term Issuer Credit Rating of “a+” (excellent) with stable outlooks.

More news:

Women in Insurance Summit speakers announced

FMA looking for a Senior Adviser, Insurance

Partners Life to release Quote for Alteration Phase 2

Partners Life new upgrade to their Quote for Alteration (QFA) digital tool is coming soon.

Partners Life new upgrade to their Quote for Alteration (QFA) digital tool is coming soon. There’s a handy tutorial here. The upgrade will provide a fully digital process, where advisers can apply for increases and alterations for existing clients in the same way they do for new clients within QFA. QFA applications will be available on Partners Protection Plan and Business Protection Plan policies; Funeral Plan, Essential, Heritage and Loancare policies cannot be serviced online through QFA.

More news:

AIA extend their 3 months' insurance free offer until 31 March 2025

AIA are introducing digital arrears notifications

AIA increases pricing for some Trauma products

AIA introduce SovLink microlearning

Fidelity Life simplify underwriting process

Partners Life paid out 93% of claims in the year ending March 31, 2024

Government commissions two independent reviews to improve the performance and sustainability of ACC

EY release global insurance outlook for 2025

EY have released their global insurance outlook for 2025, with a range of insights applicable to the health and life insurance sectors.

EY have released their global insurance outlook for 2025. One of they key takeaways for life and health insurers is the growing global retirement savings gap. Longer lifespans and aging populations are set to increase the gap from US$106 trillion in 2022 to US$483 trillion in 2025, with EY predicting increased demand for financial estate planning services, life insurance, health insurance and wellness programmes.

AI is shifting business practices globally, with 99% of insurers already investing in GenAI or making plans to invest. EY posit that as data and tech become so much more important, they must be baked into front line operations and decision-making processes. More than half of workers believe GenAI will positively impact their productivity and ability to do high-value work. EY highlight the importance of having staff with AI skills and fostering a culture of innovation and adaptability to drive productivity gains and increase employee engagement.

EY predict a rise in personalised offerings, driven in part by advances in AI helping with tailored messaging, targeted recommendations, more accurate pricing and faster underwriting. EY suggest that product innovation will prioritise features (such as preventative services) that drive outcomes customers desire (e.g. healthier lifestyles), a la AIA’s vitality programme. They also highlight that importance of partnerships and new channels to gain access to new customer segments.

More stories:

Curated Risk merges with Long Burroughs Limited

New Zealand Home Loans appoints Michelle Vaughan as Insurance Lead

Asteron Life ratings updated after sale to Resolution Life

Nick Hakes talks about Financial Advice NZ’s annual conference

mySolutions webinar 'An app solution for your FAP ' 19 February

The household living-costs price indexes increased 3.0% in the 12 months to December 2024

Changes to Fidelity Life’s executive leadership team

Fidelity Life have announced some changes to their executive leadership team. They have split the current Chief Insurance Officer into two roles. Seema Bangera will take on the role of Chief Claims Officer and Dave Winspear will take on the role of Chief Operating Officer.

Fidelity Life have announced some changes to their executive leadership team. They have split the current Chief Insurance Officer into two roles. Seema Bangera will take on the role of Chief Claims Officer and Dave Winspear, currently Head of Individual Life, will take on the role of Chief Operating Officer. Both will join the executive leadership team on 24 February. Niall McConville, Chief Insurance Officer is returning to Melbourne but will continue in a consultancy role.

Seema Bangera, Chief Claims Officer

Bangera joins from Asteron Life, where she has been Executive Manager of Claims and Customer Solutions. Bangera has 20 years experience in the industry, having held roles at Kiwibank, Westpac and HSBC.

David Winspear, Chief Operating Officer

Winspear’s responsibilities will include underwriting, new business and service to Fidelity Life’s customers and advisers and strategic partners.

Fidelity Life is currently recruiting for a new Head of Individual Life to fill the gap left by Winspear’s promotion.

Fidelity Life CEO Campbell Mitchell said

“Claims is fundamental to why we exist for our customers – it’s our purpose, to stand beside our customers when they need us most. There is a huge advantage of having a strong claims voice representing customers at the executive table to ensure customers and businesses get the support and experience they deserve during the most challenging times in their lives.”

More news:

FMA believes some FAP's compliance approach is too conservative

Financial Advice NZ Markets Summit 2025 on 19 February

Financial Advice NZ webinar 'Retirement Expenditure Guidelines' 26 February

Poll finds higher rate of life insurance policy cancellations over the past 12 months

Changes on the horizon for Fidelity Life

Fidelity Life is set to release a suite of enhancements and programmes over the next couple of months.

Fidelity Life is set to release a suite of enhancements and programmes over the next couple of months. In a video featuring Campbell Mitchell, CEO and Bronwyn Kirwan, Chief Commercial Officer, Bronwyn mentions in a couple of weeks changes will be made to underwriting processes to make it easier for customers.

The invite-only Grow Together programme, which aims to provide market-leading support across key contact areas, with dedicated support resources, will be launching in February. More information will be released in the coming weeks.

Registrations are open for Group IQ, a quarterly digital communication with the latest industry news, and Group HQ, an annual onsite conference for the top 30 groups advisers offering tailored content, expert speakers and networking opportunities.

More news:

Survey of KiwiSaver members finds they’re open to increasing the minimum contribution rate

The FMA's 2025 fintech regulatory sandbox pilot is about to launch

Fidelity Life announce product enhancements and digital, service, and retention initiatives

At Fidelity Life’s Engage 2024 conference, Fidelity Life announced a range of product enhancements, digital, service and retention initiatives and other news.

Trauma and Life covers: The entry eligibility for the Inbuilt Child’s Trauma benefit has been reduced from two years to three months, allowing more families to receive early protection. A new, separate benefit specifically for newborns facing trauma has also been introduced. Fidelity Life will also trail a premium discount for defined exclusions on trauma covers in the coming months.

Condition Definitions: Refinements have been made for clarity, and Terminal Illness has been introduced as a defined condition across the trauma range, including Child's Trauma.

Bereavement and Child’s Funeral Benefits: The Bereavement Benefit has been increased from $15,000 to $25,000, and the Child’s Funeral Benefit has been increased from $3,500 to $15,000 for children aged 10 to 20.

Grief Counselling Benefit: A new benefit offering an additional $2,500 to the sum insured.

Financial Planning Benefit: Easier access by removing thresholds and extending the claim period.

New Specific Injury Cover: A low-cost solution that pays a lump sum for any of 30 defined injuries.

Live Chat: Quick and easy access to New Business and Underwriting teams via Adviser Centre.

New-Look E-App: A modern and intuitive user experience launching in March 2025. The E-App’s latest upgrade goes live later this month, with the new ‘share’ feature enabling advisers to send a link to their customers, allowing customers to complete all or part of the application on their own.

Dedicated Adviser Service Team: A team committed to servicing all adviser needs.

Enhanced Retention Tools: Including renewal reminders and automated SMS reminders for customers. There will be additional roles created too.

Expanding adviser support roles: Fidelity Life are creating new roles, including a National Partnership Manager for mid-sized and corporate firms, as well as an Auckland Business Manager and a Desk-Based Business Manager, to provide more tailored support and drive closer engagement.

Adviser Edge Programme: New additions to the programme include an invitation-only overseas study tour and new practice manager masterclasses for admin staff.

Grow Together programme: Coming in early 2025, the invitation-only Grow Together programme will provide dedicated, prioritised support across key areas including new business, underwriting, and retention. Advisers in the programme can expect to benefit from dedicated support resources, exclusive benefits, and access to a wide range of support tools and professional development opportunities.

Adviser Council: Fidelity Life are inviting advisers to express their interest in joining their Adviser council, which meets quarterly with Fidelity Life’s leadership team to discuss industry updates, share market trends, and provides objective feedback on their initiatives.

Adviser relationship survey: To better understand market perceptions and Fidelity Life are launching a bi-annual Adviser relationship survey to provide key insights into advisers' experiences and expectations and where Fidelity Life need to improve.

Group Solutions enhancements: From early 2025, Fidelity Life will be launching a quarterly industry insight, Group IQ; holding an annual onsite Group HQ conference for the top 30 group advisers; and launching a new group solution designed for small businesses, providing enhanced tools and technology for a smoother experience and better outcomes.

Bronwyn Kirwan, Fidelity Life's Chief Commercial Officer, said

"We are thrilled to introduce these new product enhancements and initiatives. They are a testament to our ongoing commitment to providing our advisers and customers with the best possible support and value.

These enhancements deliver more value, greater accessibility, and increased choice."

More info:

Chubb Life change underwriting process for Mortgage Repayment Cover

Partners Life are holding Summer Roadshows in November & December

AIA has launched new Specified Accidental Injury Cover product

AIA survey advisers around the need for terminal illness cover

AIA Vitality members can get up to 40% off Garmin and New Balance

The FSC has recorded a small deficit of almost $46,000 before tax over the 12 months to June 30

ICNZ has welcomed the passage of the Contracts of Insurance Bill

Financial Advice NZ's national adviser conference is on 1 - 3 April 2025

mySolutions webinar 'Why Chubb?' 27 November

Lyka Burr & Vincent Zhang join TAP's compliance and governance team

Unimed offer psychologist led introductory sleep workshops

Ashleigh Buchanan from Southern Cross Health Insurance named Emerging Leader of the Year

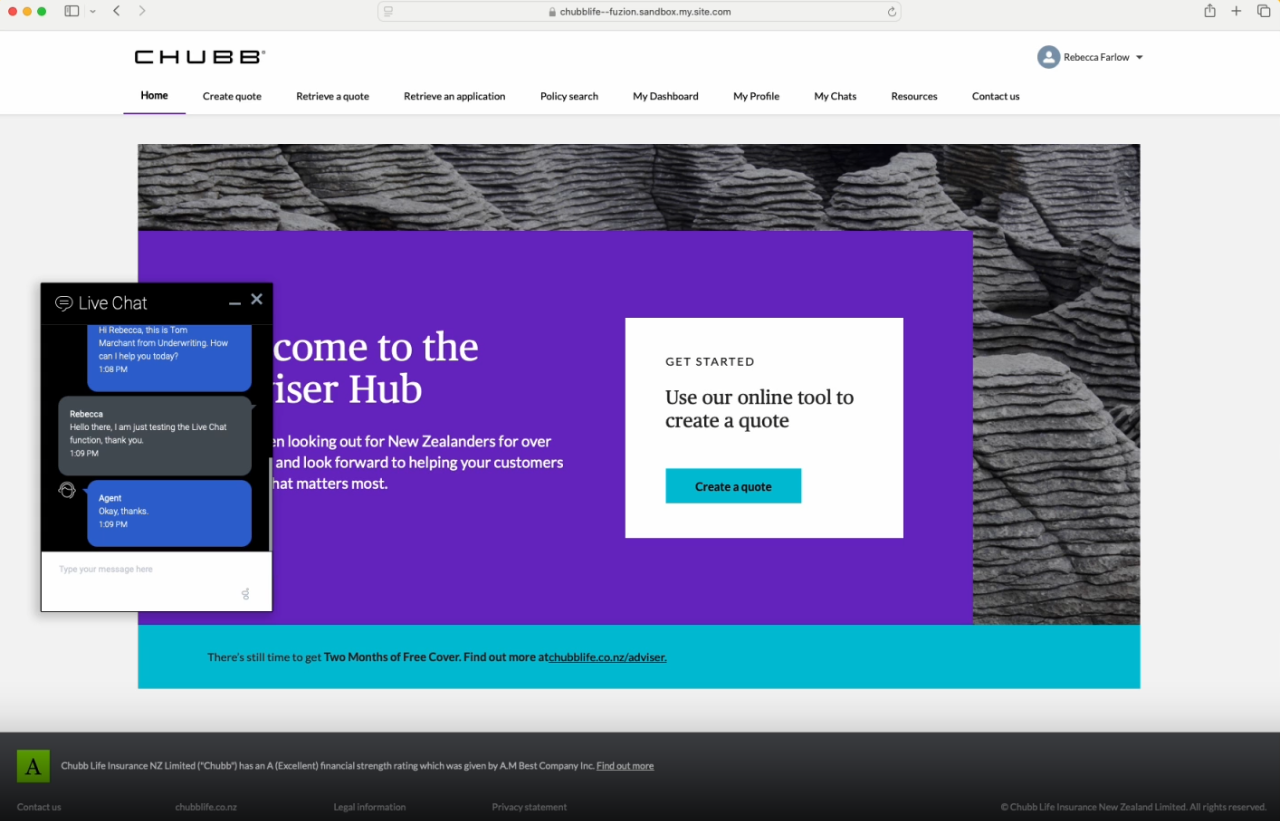

Chubb launches underwriting chat service

Chubb has launched a new chat function on their adviser hub site that allows advisers to ask the underwriting team questions.

Chubb has launched a new chat function on their adviser hub site that allows advisers to ask the underwriting team questions. Once the conversation is completed a chat transcript is able to be downloaded, for advisers to submit with the application or save to their customer files. You can find out more on their quick guide and their explainer video.

More news:

AIA NZ appoints Aaron Gilmore to the role of Regional Sales Manager – Northern

Asteron Life release their climate-related disclosures

AIA have updated their Change of Ownership forms

Hamish Patel has been elected to the board of Financial Advice NZ

FinTech NZ Hui Taumata is on 11 March 2025 in Auckland

mySolutions webinar 'Managing compliance using Sharepoint' 6 November

More than 7,500 people made early KiwiSaver withdrawals during September